- myFICO® Forums

- Types of Credit

- Credit Cards

- Re: AU or not?

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

AU or not?

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2011

05:43 AM

05-06-2011

05:43 AM

AU or not?

DD just got discover card. Would adding me as an AU negatively effect me? I just got my first card ( mtvU citi) last month. Advice?

Forward, Zync, Freedom, BofA Cash Rewards

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Message 1 of 10

0

Kudos

9 REPLIES 9

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2011

06:35 AM

05-06-2011

06:35 AM

Re: AU or not?

Since you already have a new, active and clean revolving trade line my guess is that you won't see any benefit right now. After the new account ding wears off in 6-12 months it might be worth i then.

Two questions though:

- How many total and active trade lines are on your credit reports?

- What is your AAoA (Average Age of Accounts) -- this is the average age in years for all trade lines reporting (open and closed) on your credit report?

Message 2 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2011

08:09 AM

05-06-2011

08:09 AM

Re: AU or not?

I currently have one student loan of 8 months and the new card. My AAoA would be 4.5 months I believe according to the calculation.

Forward, Zync, Freedom, BofA Cash Rewards

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Message 3 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2011

12:30 PM

05-06-2011

12:30 PM

Re: AU or not?

That new Discover (AU) won't help your score - being it's new. Now if you were added as an AU to a card that is dated back longer than your current AAoA, than it would help your score somewhat. By how much? I really don't know. But having a long AAoA are always positives in the Fico scoring.

Message 4 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2011

05:42 PM

05-06-2011

05:42 PM

Re: AU or not?

So as far as AAoA it wouldn't help, but what about futute CLs? My current CL on the mtvU card is $800. The Discover Card is $10,500. Does anyone see larger CLs because i am an AU on an account with a higher limit or does that have no affect?

Forward, Zync, Freedom, BofA Cash Rewards

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Message 5 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2011

07:58 PM

05-06-2011

07:58 PM

Re: AU or not?

Shouldn't affect you at all.

TW=825, CB=819, TU=946

Message 6 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-07-2011

02:06 PM

05-07-2011

02:06 PM

Re: AU or not?

So being an AU on a high cl card doesn't help your own?

Forward, Zync, Freedom, BofA Cash Rewards

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Current Score: 738 BOA Experian (5/29/2012)

GOAL: 800s

Message 7 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-08-2011

12:39 PM

05-08-2011

12:39 PM

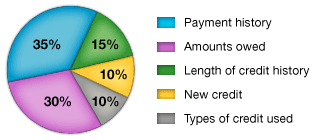

Re: AU or not?

The above chart of the makeup of Fico scoring is from this page.

Adding DD's CC will immediately do three things to your reports:

1) It will increase your total credit limits -- which may help or hurt your credit score depending on DD's usage.

2) It will add a clean trade line -- which may help your credit score.

3) It will add a brand new account -- which may hurt your credit score for the next 6-12 months.

By adding the card as an AU, you are giving up a little control over your credit history (which can be removed if the trade line goes sour by removing yourself as an AU):

1) If DD spends a lot and doesn't pay before the statement cuts, or if she carries a balance, that can increase your utilization -- which would decrease your score.

2) You also inherit the payment history of the card. If DD is a responsible user of credit, you should benefit as she makes charges and payments on the card without being late.

In short, you inherit all the good and all the bad when you become an AU.

If you plan on applying for new credit in the next 6-12 months, adding this trade line might help you or hurt you. After 12 months, if it's clean (no late payments) with low utilization it will most likely help you a lot.

In terms of helping you get higher CLs, there's really no way to know how adding you as an AU to a higher CL card will help you. For DW (as an example), Chase wouldn't budget past a $600 CL (despite being an AU on clean trade lines totaling $55,600) while Amex gave DW a $5,500 CL the next day last summer.

While most CC issuers use Fico scores, almost every issuer has their own underwriting process beyond Fico scores to determine approvals and CLs.

Message 8 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-08-2011

02:06 PM

05-08-2011

02:06 PM

Re: AU or not?

Can I hijack this thread real quick? I have the same question and then some. What's better joint account or AU? It's my dad so I'm not worried of getting stuck with the bill. It would be his American Express. The only issue is...well he's had this account since 83. I was born in 89. Is that an issue because I feel like it would be. And I also read somewhere that being an AU doesn't effect your actual score. That it just shows up on your credit report.

Starting Score: EX 631 EQ 629 TU 646 1/18

Starting Score: EX 631 EQ 629 TU 646 1/18

Current Score: __

Goal Score: 710

Take the FICO Fitness Challenge

Current Score: __

Goal Score: 710

Take the FICO Fitness Challenge

Message 9 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-08-2011

09:18 PM

05-08-2011

09:18 PM

Re: AU or not?

@bearsfan --

Unless you're married to them, AU. Plain and simple answer.

Here's where this gets fun. After you become an AU, wait until the card reports on your credit report. Then, if you've never had an Amex card before, go apply for your own Amex card. You should now have an open date of the month you apply in 1983 -- you may have to make some calls to ensure you get the backdating.

There's no guarantee Amex will backdate a tradeline, but dozens of people here on the boards have been successful -- including DW.

Message 10 of 10

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.