- myFICO® Forums

- Types of Credit

- Credit Cards

- Fico is telling me it is hurting my score. I dont ...

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

First Premier

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- « Previous

-

- 1

- 2

- Next »

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

09:48 PM

01-06-2013

09:48 PM

Re: First Premier

Can you explain a little more about how the average age of the acounts is not affected?

Also there seems to be 2 categories 1 average age all credit history which mine lists as a positive on my credit report.

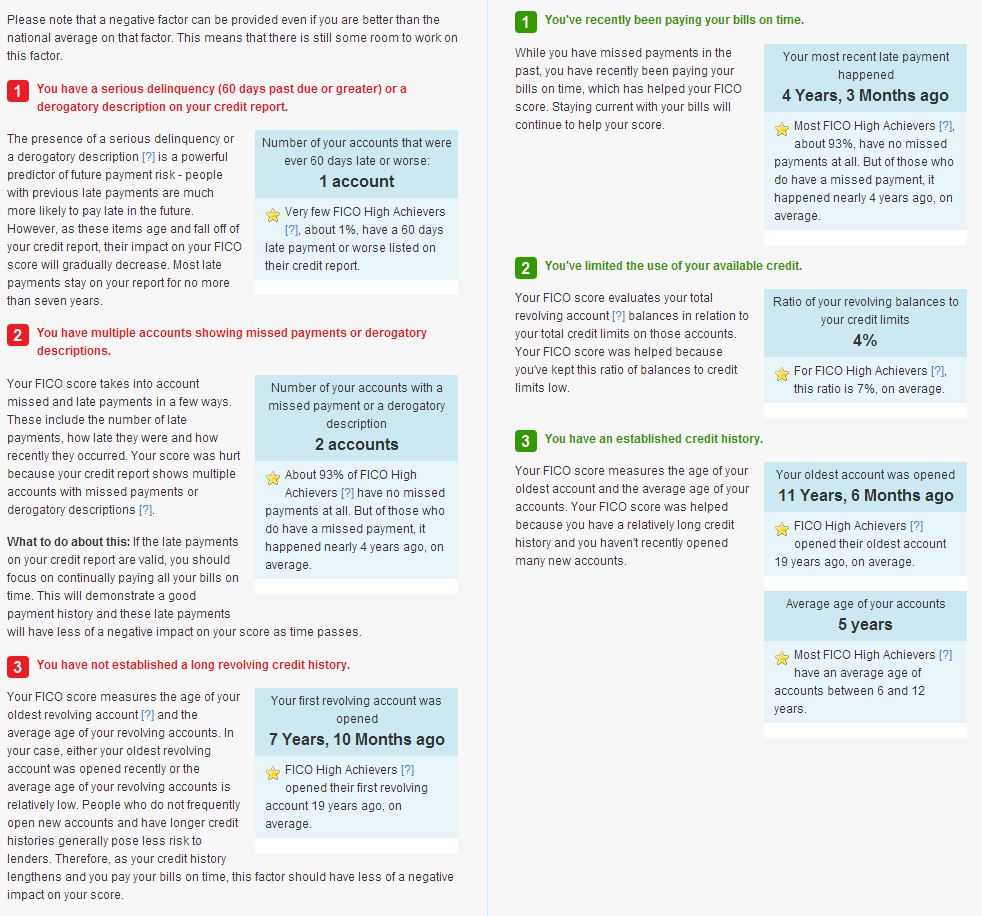

Then there seems to be a second which is the age of your revolving credit accounts. It says my oldest account or the average age of my revolving credit is hurting my score. It says my oldest account is 7 years 10 months old, but doesn't list the average age of my revolving accounts.

Thanks,

Mike

Message 11 of 19

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

09:54 PM

01-06-2013

09:54 PM

Re: First Premier

@Anonymous wrote:Can you explain a little more about how the average age of the acounts is not affected?

Also there seems to be 2 categories 1 average age all credit history which mine lists as a positive on my credit report.

Then there seems to be a second which is the age of your revolving credit accounts. It says my oldest account or the average age of my revolving credit is hurting my score. It says my oldest account is 7 years 10 months old, but doesn't list the average age of my revolving accounts.

Thanks,

Mike

See the sticky at the top of the forum, Closing Credit Cards: http://ficoforums.myfico.com/t5/Credit-Cards/Closing-Credit-Cards/td-p/347190

Summary at end:

In the short-term, there should be no adverse affect to your FICO scores, average age of accounts, or the length of your credit history, provided there is no increase in your util% calculations after you close any CC(s). In the long-term, a CC in good standing (nothing derogatory reporting) with a $0 balance will generally be deleted from your CRs (credit reports) after 10 years. Once this account is deleted, you lose the history and age of this TL and this might lower your scores.

Basically, closed accounts continue to report for up to ten years (and sometimes more). Otherwise people would just close accounts with lates etc and baddies would go away. So your average age of accounts continues to age, with both open and closed accounts. While open accounts should always be on the report, closed accounts drop off eventually, either automatically, 10 years after CLOSURE, or, in some cases, the lender purges inactive accounts from their records, and then these no longer appear on the credit report. This will still usually be years rather than months.

But closing an account can impact utilization, which can drop your score. In the case here, that won't happen because the closed account has such a small CL.

Message 12 of 19

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

09:57 PM

01-06-2013

09:57 PM

Re: First Premier

Please also answer why so many people say that you should keep the account open for at least a year, then cancel it before the AF hits. It seems like it doesn't even matter when you close it. It is still going to report for 10 years right?

My Wallet:

WalMart: ||15k|| USAA Platinum MC: ||26k|| BCE: ||9k|| Chase Freedom Siggy: ||10k|| Discover it: ||6.5k|| SG Visa: ||11k||

USAA World MC: ||23k|| US Bank Cash+ Siggy: ||7.5k|| Citi TYP World MC: ||12k|| Barclays Arrival World MC: ||13k||Citi Double Cash World MC ||25k||Sallie Mae World MC ||18.8k||Fico Scores (3 Fico Monitoring): EQ 751,TU 749, EX 743. Last app: 9-12-14 Sallie

Message 13 of 19

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

10:08 PM

01-06-2013

10:08 PM

Re: First Premier

@Swapmeet wrote:Please also answer why so many people say that you should keep the account open for at least a year, then cancel it before the AF hits. It seems like it doesn't even matter when you close it. It is still going to report for 10 years right?

Differing views from people at different stages of credit! But to try to present a balanced view:

1) As you say, closing it at any time won't impact AAoA in the short/medium term. The clock ticks from the time it is closed, so keeping for almost one year will keep it on the record (more or less) for 11 years, whereas closing it the first week would keep it only for 10. But hopefully in either 10 or 11 years, your finances are quite different anyway!

2) The myFico obsessive view (OK, so much for balance!) Here the point is that you have taken the hard pull to get the card and so you may as well get value from it. Depending on the card, people will also suggest that you get a CLI during this first year to improve score and maybe make other issuers match

3) Safety: Some issuers are wary of people who only sign up for bonuses and then don't use/cancel the card. Having cards open and closed in a short period of time is a sign of this, so even if you have good reason (misunderstood the terms of the card etc) closing it early might raise red flags with issuers you really care about.

Same applies when applying for a mortgage, an underwriter might ask questions about any unusual behavior. Your job is to avoid behavior that raises these questions.

Message 14 of 19

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

10:17 PM

01-06-2013

10:17 PM

Re: First Premier

Sorry I'm a bit skeptical. If the average age of my revolving account includes closed accounts then my average is over 5 years would this really hurt my credit? 5 years is listed as a positive on my complete credit history AAoA. This includes a couple store cards, but even if its only major credit cards then its still over 4.5 years. For just my 3 open accounts now the average is 3.7 years. I think possibly complete credit history AAoA isn't affected but the average age of revolving accounts is.

Message 15 of 19

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

10:23 PM

01-06-2013

10:23 PM

Re: First Premier

@Anonymous wrote:Sorry I'm a bit skeptical. If the average age of my revolving account includes closed accounts then my average is over 5 years would this really hurt my credit? 5 years is listed as a positive on my complete credit history AAoA. This includes a couple store cards, but even if its only major credit cards then its still over 4.5 years. For just my 3 open accounts now the average is 3.7 years. I think possibly complete credit history AAoA isn't affected but the average age of revolving accounts is.

Skeptical about what? What does your Credit Report show for Average Age of Accounts, as that is what goes into your FICO score? So, yes, we are talking about complete credit history AAoA. Average Age of Revolving accounts would be impacted if it only counts open ones of course, but I don't know what considers that as a factor.

Message 16 of 19

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

10:45 PM

01-06-2013

10:45 PM

Re: First Premier

I'm skeptical that it doesn't affect the average age of my revolving accounts. You are talking about my complete credit history AAoA, I stated that I was talking about the age of my revolving accounts which is listed as a negative on my credit report.

For my complete credit history it lists the average age of accounts as 5 years and its listed as a positive.

It doesn't list the average age of my revolving account just that my oldest revolving credit is 7 years and 10 months(This could also be young but I wouldn't think 7 years as a negative, at least neutral, maybe even positive).

This is what it says under the negative:

"Your FICO score measures the age of your oldest revolving account and the average age of your revolving accounts. In your case, either your oldest revolving account was opened recently or the average age of your revolving accounts is relatively low. People who do not frequently open new accounts and have longer credit histories generally pose less risk to lenders. Therefore, as your credit history lengthens and you pay your bills on time, this factor should have less of a negative impact on your score."

Message 17 of 19

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-06-2013

11:04 PM

01-06-2013

11:04 PM

Re: First Premier

OK, I can just point to the stuff above, or, for example: http://www.bankrate.com/finance/credit-cards/closing-credit-card-dings-credit-score-2.aspx from a Fico Product Manager:

An account that is open with a good history can stay on forever -- it could stay on for 20 years. The bureaus will automatically remove (a closed account) in 10 years, but that could be removed sooner if that credit card issuer decides to remove it. Once it's closed and paid off, that account then becomes inactive, and it's not uncommon for the credit card issuer after a few years or even sooner to just delete that completely, just purge it from their records.

In the short run, you maintain that history. But once that comes off your credit report, you lose that good history. One of those five areas that the score considers looks at how long you've had credit -- that accounts for about 15 percent of the score. That may or may not impact your score a lot depending on your other accounts. If you've only got a few accounts, that could impact it heavily; if you've got a lot of credit for a long period of time, that will probably not impact it by much, if at all.

So do you have evidence that it impacts the FICO score? I would expect closed and open to be treated the same way throughout. On my report it talks about the oldest revolving credit line, but average age of accounts (not revolving accounts). Not sure why it is different from what you have

Message 18 of 19

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-07-2013

01:11 AM

01-07-2013

01:11 AM

Fico is telling me it is hurting my score. I dont know ho...

@bs6054 wrote:OK, I can just point to the stuff above, or, for example: http://www.bankrate.com/finance/credit-cards/closing-credit-card-dings-credit-score-2.aspx from a Fico Product Manager:

An account that is open with a good history can stay on forever -- it could stay on for 20 years. The bureaus will automatically remove (a closed account) in 10 years, but that could be removed sooner if that credit card issuer decides to remove it. Once it's closed and paid off, that account then becomes inactive, and it's not uncommon for the credit card issuer after a few years or even sooner to just delete that completely, just purge it from their records.

In the short run, you maintain that history. But once that comes off your credit report, you lose that good history. One of those five areas that the score considers looks at how long you've had credit -- that accounts for about 15 percent of the score. That may or may not impact your score a lot depending on your other accounts. If you've only got a few accounts, that could impact it heavily; if you've got a lot of credit for a long period of time, that will probably not impact it by much, if at all.

So do you have evidence that it impacts the FICO score? I would expect closed and open to be treated the same way throughout. On my report it talks about the oldest revolving credit line, but average age of accounts (not revolving accounts). Not sure why it is different from what you have

Thanks for the link. Fico is telling me it is hurting my score. I dont know how much at this point though. Like I said it could be that 7 years is too short as well, because it doesn't list what my average age of my revolving accounts actually is.

Message 19 of 19

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.