- myFICO® Forums

- Types of Credit

- Credit Cards

- How do you rack up YOUR points?

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

How do you rack up YOUR points?

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-10-2016

08:44 PM

07-10-2016

08:44 PM

Re: How do you rack up YOUR points?

@Anonymous wrote:I only have 1 travel card so far, but I have a pretty good idea of what my strategy will be when I get more. For me it's not about the bank but the travel partners. For example, Chase's UR program does not appeal to me because I mainly fly Delta. I also don't stay in hotels, I'm in my mid-20's and stay in hostels when I travel. I never fly United, so the only reason I'd get the Sapphire Preferred/United card is if I wanted to fly on United's partners, such as SWISS Air, an airline I do fly. So other than when I go for big sign up bonuses in the future, I'll keep it within AmEx/Membership Rewards, so I can transfer them to Delta.

Chase UR just added Flying Blue as a transfer partner. Flying Blue is closely aligned with Delta, so by transferring points to FB, you either get a better redemption of those points to Europe, or a good / better redemption on US domestic flights that in many cases are fulfilled by Delta. This does not directly add to your Delta miles, only MR points ( and the not-available Diners card ) do the direct transfer, but as a use of UR points, it can be an opportunity.

High Bal Jan 2009 $116k on $146k limits 80% Util.

Oct 2014 $46k on $127k 36% util EQ 722 TU 727 EX 727

April 2018 $18k on $344k 5% util EQ 806 TU 810 EX 812

Jan 2019 $7.6k on $360k EQ 832 TU 839 EX 831

March 2021 $33k on $312k EQ 796 TU 798 EX 801

May 2021 Paid all Installments and Mortgages, one new Mortgage EQ 761 TY 774 EX 777

April 2022 EQ=811 TU=807 EX=805 - TU VS 3.0 765

Oct 2014 $46k on $127k 36% util EQ 722 TU 727 EX 727

April 2018 $18k on $344k 5% util EQ 806 TU 810 EX 812

Jan 2019 $7.6k on $360k EQ 832 TU 839 EX 831

March 2021 $33k on $312k EQ 796 TU 798 EX 801

May 2021 Paid all Installments and Mortgages, one new Mortgage EQ 761 TY 774 EX 777

April 2022 EQ=811 TU=807 EX=805 - TU VS 3.0 765

Message 11 of 22

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-10-2016

08:50 PM

07-10-2016

08:50 PM

Re: How do you rack up YOUR points?

@Anonymous wrote:Do you spread out your points / credit cards with a whole bunch of different companies? Or do you try to keep it within one or two companies? Which do you prefer & why?

Debating to focus more on TYP, UR, or Cashback & would like to hear all of your wonderful experiences & opinions 😊😊

Which cards do you have already? Which airlines do you prefer to fly with? Hotel programs?

There are many possibilities, but the question should start from what is best for your travel plans, and understanding the existing cards you have in your wallet. From there you can determine whether adjustments are necessary, or if you are already well on your way. The question of annual fees is also important: several cards have an AF, and you will want to decide if the benefits of the AF make it worth keeping a particular card long term make sense.

For example, Flying Blue is a transfer partner for both TYP and UR, so that might be a place to combine the points.

It is also relevant to let us know the cards you already have, because that does influence what some of your options are.

High Bal Jan 2009 $116k on $146k limits 80% Util.

Oct 2014 $46k on $127k 36% util EQ 722 TU 727 EX 727

April 2018 $18k on $344k 5% util EQ 806 TU 810 EX 812

Jan 2019 $7.6k on $360k EQ 832 TU 839 EX 831

March 2021 $33k on $312k EQ 796 TU 798 EX 801

May 2021 Paid all Installments and Mortgages, one new Mortgage EQ 761 TY 774 EX 777

April 2022 EQ=811 TU=807 EX=805 - TU VS 3.0 765

Oct 2014 $46k on $127k 36% util EQ 722 TU 727 EX 727

April 2018 $18k on $344k 5% util EQ 806 TU 810 EX 812

Jan 2019 $7.6k on $360k EQ 832 TU 839 EX 831

March 2021 $33k on $312k EQ 796 TU 798 EX 801

May 2021 Paid all Installments and Mortgages, one new Mortgage EQ 761 TY 774 EX 777

April 2022 EQ=811 TU=807 EX=805 - TU VS 3.0 765

Message 12 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

12:30 PM

07-11-2016

12:30 PM

Re: How do you rack up YOUR points?

I only have a few cards so I'm limited on that lol. I have two 5% rotating category cards, so I reserve my monthly spending on a certain category for those cards. I signed up for QS for the cash bonus and no FTF, and want to get it to at least 5k limit so I'll be putting all other spending on it for 1.5% back. Right now I'm just putting recurring charges (like certain bills) on my DC 2%, but I'll be using it for all general spending (once I bump my QS up) except for anything out of the US ![]()

I maximize rewards, doesn't matter what company. But I do want to get all my limits to at least 5k, so that's also a factor on what cards I focus on.

Message 13 of 22

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

12:37 PM

07-11-2016

12:37 PM

Re: How do you rack up YOUR points?

@Anonymous wrote:Most of my spend is on the Chase cards for UR points. I chose this becuase they seem the most flexible for redemption with different arlines and hotels. I use my Amex blue cash whenever they have a good promo for the card, like 10% off gas right now. I chose one system , UR, becuase I don't want to have points spread all over the place and have to keep track of where they are.

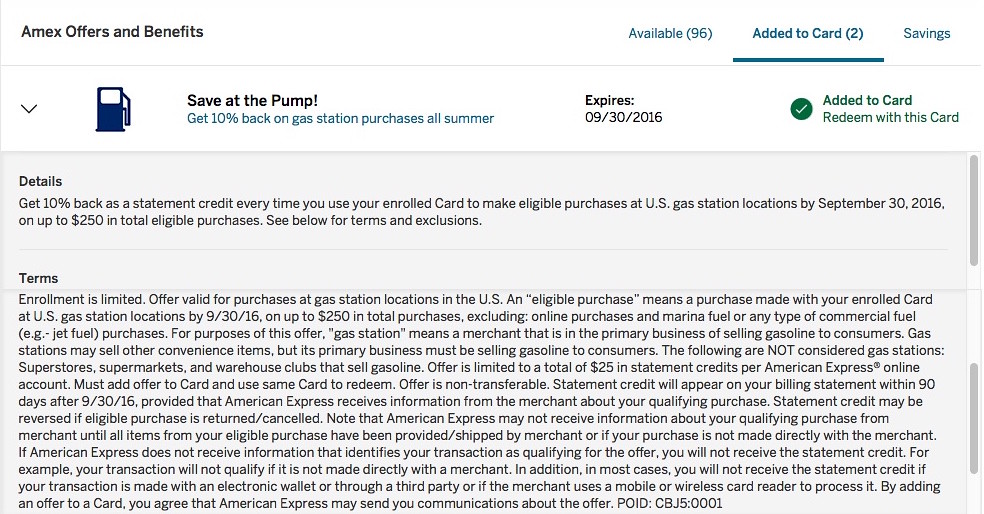

When did Amex start offering 10% on gas? The only 10% i have seen is on wireless

$325k Total Limits, 4% Util

Message 14 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

12:52 PM

07-11-2016

12:52 PM

Re: How do you rack up YOUR points?

Freedom & Discover It are strictly for categories. Citi hilton & CSP are used when I travel, shopping and any other big purchases. My QS MC is my main for reoccuring charges but I have been thinking long and hard to switch it and divide it to my CSP and Citi HH. My QS VS is used by my brother who is an AU while he is away for college. BOA cash rewards gas and groceries.

Message 15 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

01:50 PM

07-11-2016

01:50 PM

Re: How do you rack up YOUR points?

My primary source of reward is UR. I cashed it all out before. It didn't matter when I didn't have a CSP but since I do now, I try to save all my UR points for a free flight.

Message 16 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

02:00 PM

07-11-2016

02:00 PM

Re: How do you rack up YOUR points?

ALL through chase!

Message 17 of 22

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

06:11 PM

07-11-2016

06:11 PM

Re: How do you rack up YOUR points?

For me, I'm juggling between TY, MR and TrueBlue points. I maximize my spend based on what gives me the highest reward/most value for my next redemption.

Currently it's Access more and Premier combo for 3x TY online purchases, travel and gas. JetBlue plus for 2x TrueBlue points restaurants/groceries. AMEX ED for everything else.

Currently sitting on 130k MR, soon to be 50k TY and 115k TrueBlue points.

I want to build up my TY points a bit more and then apply for SPG to up my starpoint game. I have a measely 6k there. Those starpoints are hard to come by without heavy CC spend which I plan to do a lot of.

")

Currently it's Access more and Premier combo for 3x TY online purchases, travel and gas. JetBlue plus for 2x TrueBlue points restaurants/groceries. AMEX ED for everything else.

Currently sitting on 130k MR, soon to be 50k TY and 115k TrueBlue points.

I want to build up my TY points a bit more and then apply for SPG to up my starpoint game. I have a measely 6k there. Those starpoints are hard to come by without heavy CC spend which I plan to do a lot of.

Message 18 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

07:54 PM

07-11-2016

07:54 PM

Re: How do you rack up YOUR points?

sdchrgrboy wrote: When did Amex start offering 10% on gas? The only 10% i have seen is on wireless

I think they started offering it at the end of June.

Message 19 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

07-11-2016

07:57 PM

07-11-2016

07:57 PM

Re: How do you rack up YOUR points?

@NRB525 wrote:

@Anonymous wrote:I only have 1 travel card so far, but I have a pretty good idea of what my strategy will be when I get more. For me it's not about the bank but the travel partners. For example, Chase's UR program does not appeal to me because I mainly fly Delta. I also don't stay in hotels, I'm in my mid-20's and stay in hostels when I travel. I never fly United, so the only reason I'd get the Sapphire Preferred/United card is if I wanted to fly on United's partners, such as SWISS Air, an airline I do fly. So other than when I go for big sign up bonuses in the future, I'll keep it within AmEx/Membership Rewards, so I can transfer them to Delta.

Chase UR just added Flying Blue as a transfer partner. Flying Blue is closely aligned with Delta, so by transferring points to FB, you either get a better redemption of those points to Europe, or a good / better redemption on US domestic flights that in many cases are fulfilled by Delta. This does not directly add to your Delta miles, only MR points ( and the not-available Diners card ) do the direct transfer, but as a use of UR points, it can be an opportunity.

You can also transfer UR points to Kroean Air then on to Delta.

Message 20 of 22

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.