- myFICO® Forums

- Types of Credit

- Credit Cards

- Refinance or Balance Transfer ?

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Refinance or Balance Transfer ?

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- « Previous

-

- 1

- 2

- Next »

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-22-2015

11:23 AM

08-22-2015

11:23 AM

Re: Refinance or Balance Transfer ?

True citi may not give checks. For bt. But they let you write chevk to yourself. To use any which way you want. At 0% as well. Op myni can save in interest. Just make higher payments. Make sure the overage girs to principal. Nthen de even lower interest. Suzie orman does not know your credit score. You can go either way. Just saying. Hurting score can cost money too.

Message 11 of 18

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-22-2015

12:32 PM

08-22-2015

12:32 PM

Re: Refinance or Balance Transfer ?

There's no guarantee chase slate could get that high even with combining. And they can double pull. I would think your credit mix would be better from a auto loan refi with nasa.

Message 12 of 18

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-22-2015

12:47 PM

08-22-2015

12:47 PM

Re: Refinance or Balance Transfer ?

@Anonymous wrote:There's no guarantee chase slate could get that high even with combining. And they can double pull. I would think your credit mix would be better from a auto loan refi with nasa.

Ive opened Nasa last year because was soft pull then they denied me for their credit card so i didnt want to press my luck getting hard pulled so i left it alone after that. But i am still a member at Nasa credit union but their starting rates are higher than Digital Credit Union and Pennsylvania state employees credit union so i didnt include Nasa as an option for refinancing my current $7,500 auto loan with wells fargo which sits at 6.99% 3 years left to go on a 60 month (5 year term).

Message 13 of 18

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-22-2015

05:52 PM

08-22-2015

05:52 PM

Re: Refinance or Balance Transfer ?

@Anonymous wrote:

@NRB525 wrote:

@taxi818 wrote:With that rate. Don't kniw why you are worrying of it. No BT is going yo last 36 months. Even if 0%. Also that's hoping you get a card with limit that high. Then maxing it with a bt. If your scores are outstanding even more than what it was when you got car will be tough to refinance for lower than you have on a used car. But does not hurt to try. But if you are raising your payments say on slate you coukd leave it alone. Pay the same amount now that you want to pay on slate. Which will go to principal. And be done in same amount of time. Without hurting score. But you have many options outlined. Either is fine.

+1

OP, you have all kinds of analysis going on here. I think you may be overthinking it. Pay the existing loan at a higher rate if you want. That keeps the installment loan on your credit file, maybe not as long, but it gets you to your pay off at the same time. And keeping the existing installment loan on your credit file is currently actually boosting your score. Go over to the Understanding FICO forum and search for "Paid off my installment loan and lost 20/30 points". There's a bunch of those. I would not be in any hurry to get rid of the installment loan.

Negotiating power if you have the title clear? Not really. The car would be sold at a price, the buyer or dealer cares not what you owe on it. The money from any sale needs to go to pay off that loan, so even if you BT, you should be planning on using any proceeds from the sale of the vehicle to pay that off, which takes all the fun out of doing the BT in the first place.

If you really insist on doing a BT to take advantage of that 2.9%, fine, transfer $2k and have fun with that.

The insurance thing? Insurance is an expense... until something happens.... and you lose your vehicle,... and you can't immediately pay off the $10k loan (or $10k balance transfer) to free up monthly payment amounts to get a new vehicle. Or pay for repairs.

You don't have Slate or Cash+ yet? I would not build in any presumptions about limits and availability if those are not in hand yet.

No i dont have chase slate yet thats why if i were to take a hard inquiry i would apply 2 chase cards for 1 hard inquiry. My freedom only $6,000 limit and its my lowest besides $500 bank america (my first credit card) which Dying to raise it or turn it into a signature visa but they wont without a har d inquiry. My

months 0% on my freedom will be up march 2016 but charges 3% Fee. Same goes for Citi. I guess yoi right. The longer the loan the better it looks on my credit report. Its a 5 year wells fargo auto loan. I have 3 years left. Suze orman says a car loan longer than 36 months (3 years) is a waste of money and one of the biggest mistakes you could make when buying a car and says its a sign of financial irresponsible so i thought maybe i should try clear it up (avoid 2 more years of interest if not 3) and pay it off now.

If I've unraveled the numbers right, it seems your original loan was for about $15,800. You've paid about $1800 in interest and have about $1100 in interest you'll pay if you continue to pay it at the same rate. Originally you were paying $90 a month in interest, you're down to paying about $60 a month in interest.

If you kick your payment up by about $100 a month, you'll only pay about $800 in interest and have it paid off about 10 months sooner.

Message 14 of 18

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-23-2015

03:30 AM

08-23-2015

03:30 AM

Re: Refinance or Balance Transfer ?

@Anonymous wrote:

@Anonymous wrote:

@NRB525 wrote:

@taxi818 wrote:With that rate. Don't kniw why you are worrying of it. No BT is going yo last 36 months. Even if 0%. Also that's hoping you get a card with limit that high. Then maxing it with a bt. If your scores are outstanding even more than what it was when you got car will be tough to refinance for lower than you have on a used car. But does not hurt to try. But if you are raising your payments say on slate you coukd leave it alone. Pay the same amount now that you want to pay on slate. Which will go to principal. And be done in same amount of time. Without hurting score. But you have many options outlined. Either is fine.

+1

OP, you have all kinds of analysis going on here. I think you may be overthinking it. Pay the existing loan at a higher rate if you want. That keeps the installment loan on your credit file, maybe not as long, but it gets you to your pay off at the same time. And keeping the existing installment loan on your credit file is currently actually boosting your score. Go over to the Understanding FICO forum and search for "Paid off my installment loan and lost 20/30 points". There's a bunch of those. I would not be in any hurry to get rid of the installment loan.

Negotiating power if you have the title clear? Not really. The car would be sold at a price, the buyer or dealer cares not what you owe on it. The money from any sale needs to go to pay off that loan, so even if you BT, you should be planning on using any proceeds from the sale of the vehicle to pay that off, which takes all the fun out of doing the BT in the first place.

If you really insist on doing a BT to take advantage of that 2.9%, fine, transfer $2k and have fun with that.

The insurance thing? Insurance is an expense... until something happens.... and you lose your vehicle,... and you can't immediately pay off the $10k loan (or $10k balance transfer) to free up monthly payment amounts to get a new vehicle. Or pay for repairs.

You don't have Slate or Cash+ yet? I would not build in any presumptions about limits and availability if those are not in hand yet.

No i dont have chase slate yet thats why if i were to take a hard inquiry i would apply 2 chase cards for 1 hard inquiry. My freedom only $6,000 limit and its my lowest besides $500 bank america (my first credit card) which Dying to raise it or turn it into a signature visa but they wont without a har d inquiry. My

months 0% on my freedom will be up march 2016 but charges 3% Fee. Same goes for Citi. I guess yoi right. The longer the loan the better it looks on my credit report. Its a 5 year wells fargo auto loan. I have 3 years left. Suze orman says a car loan longer than 36 months (3 years) is a waste of money and one of the biggest mistakes you could make when buying a car and says its a sign of financial irresponsible so i thought maybe i should try clear it up (avoid 2 more years of interest if not 3) and pay it off now.

If I've unraveled the numbers right, it seems your original loan was for about $15,800. You've paid about $1800 in interest and have about $1100 in interest you'll pay if you continue to pay it at the same rate. Originally you were paying $90 a month in interest, you're down to paying about $60 a month in interest.

If you kick your payment up by about $100 a month, you'll only pay about $800 in interest and have it paid off about 10 months sooner.

or split it and pay half of interest or less but i guess the conclusion is to just leave it alone. so now my hard inquires are reserved for either US bank cash+, a limit increase on my bank america card which sits $500 for 3 years now ![]() or take a hard inquiry and apply chase slate and sapphire (2 cards for 1 inquiry). Barclay also has a low limit (2nd lowest) which i hate because they send me these white and blue balance transfer checks. I was planning upgrading Barclay Rewards to Arrival + in the late fall using the number they gave me to call and ask if they be willing to increase the limit soft pull.

or take a hard inquiry and apply chase slate and sapphire (2 cards for 1 inquiry). Barclay also has a low limit (2nd lowest) which i hate because they send me these white and blue balance transfer checks. I was planning upgrading Barclay Rewards to Arrival + in the late fall using the number they gave me to call and ask if they be willing to increase the limit soft pull.

OPTION 3

American Express Blue Cash 0% intro for 15 months

$10,000 balance transfer

15 monthly payments of $416

$300 in fees. (3% balance transfer fee)

US Bank Cash+ 0% intro for 9 months

$3,760 balance transfer

9 monthly payments of $417

$112 in fees. (3% balance transfer fee)

----------------------------------------------------------------------------------------- 2 years carrying a balance (24 months total)

$412 total fees.

OPTION 4

Chase Slate 0% intro for 15 months

$10,000 balance transfer

15 monthly payments of $416

$0 in fees

American Heritage Credit Union 4.99% 24 months

or Valor Credit Union lifetime 5.99%

$3,760 balance transfer

24 monthly payments of $156

$184 in fees. (4.99% interest charged)

——————————————————————————— 3 years carrying a balance (39 months total)

$184 total fees (American Heritage) $221 total fees (Valor)

OPTION 5

Chase Slate 0% intro for 15 months

$10,000 balance transfer

15 monthly payments of $416

$0 in fees

Pennsylvania State Employees Credit Union 2.99% 15 months

$3,760 balance transfer

15 monthly payments of $250

$92 in fees. (2.99% interest charged)

——————————————————————————— 2.5 years carrying a balance (30 months total)

$92 total fees

Message 15 of 18

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-23-2015

08:22 AM

08-23-2015

08:22 AM

Re: Refinance or Balance Transfer ?

With car rates the way they are currently and the fact of how it is calculated into your credit... you will tank yourself for a little bit moving all that debt to a credit card and without being able to explain that to future creditors while you are still carrying the balance it just won't look good and then you will also loose the installment loan which is a big help for your credit history too!

I would refinance it to 24-36 months with a credit union as an AUTO LOAN and call it a day or as some have suggested just start paying your current auto loan on a 24 months schedule instead.

I don't see any of your calculations of your current auto loan of just paying it in 24 months as you are suggesting you would pay most of the credit card options you listed.

Compare apples to apples. but either way I wouldn't go unsecured with an auto loan unless you are in jeopardy of losing it

Message 16 of 18

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-23-2015

08:27 AM

08-23-2015

08:27 AM

Re: Refinance or Balance Transfer ?

@Anonymous wrote:

@kdm31091 wrote:I'd lean towards refinancing the loan vs putting it on a credit card. Your utilization will skyrocket, which is going to lower your score. While this is temporary (as temporary as the high util, anyway), if you're just starting out, tanking your scores may not make you feel so great. There is no compelling advantage that I see to putting it on a credit card.

the whole point of doing this was so i can be ready to sell the car at anytime. It's a 2005 vehicle. I could just give it to CarMax with a lien but i thought if I will have the title to the car that would give me negotiation power. Also if i decide to keep the car... the car insurance would be much cheaper costing me $50 a month instead of $115 i am paying now reqired by WellsFargo. Will no longer be required to have full coverage after Wells Fargo releases the lien to me.

Once i sold the car i go back and pay off the credit card i transferred the balance to. Though i would hate to put a tent on my credit even if its temporary as others have stated would not make me feel good at all. I don't think $5,000 would put much harm though. $10,000 would especially if i do not get a sufficient limit. They would have to give me $100,000 limit just to be at 10% utilization. I also like to make the most of my hard inquiries. So if i apply for Chase Slate i would apply for Chase Sapphire (2 cards for 1 inquiry). I also wanted the US Bank Cash+ recent offers sitting on the table ...18 months 0% cash rewards from WellsFargo$150 cash back Blue Cash American Express. 0% 15 months$250 cash back American Express Everyday (white card).and 100,000 points bonus American Express Platinum.Pennsylvania State Employeees Credit Union i hear to combine visa transfer card and Personal Line of Credit in which if i do not use my credit cards a PLOC will not close due to inactivity which may be good to keep my credit score from dropping (doormat) if i never use credit cards living abroad for a couple of years ? anything know about this ? Then maybe thats where i should maybe invest my hard inquires getting a PLOC instead

recent offers sitting on the table ...18 months 0% cash rewards from WellsFargo$150 cash back Blue Cash American Express. 0% 15 months$250 cash back American Express Everyday (white card).and 100,000 points bonus American Express Platinum.Pennsylvania State Employeees Credit Union i hear to combine visa transfer card and Personal Line of Credit in which if i do not use my credit cards a PLOC will not close due to inactivity which may be good to keep my credit score from dropping (doormat) if i never use credit cards living abroad for a couple of years ? anything know about this ? Then maybe thats where i should maybe invest my hard inquires getting a PLOC instead

After looking at this new information, the answer is clearly "none of the above".

You should not refinance it in any way.

You should sit still, enjoy your good rate, let the loan age, get no new inquiries, get no new accounts, and pay the loan down as fast as possible.

30k")

25k")

20k")

15k")

15k")

FCU Platinum Prime Plus MC 15k")

14k")

12k")

7k")

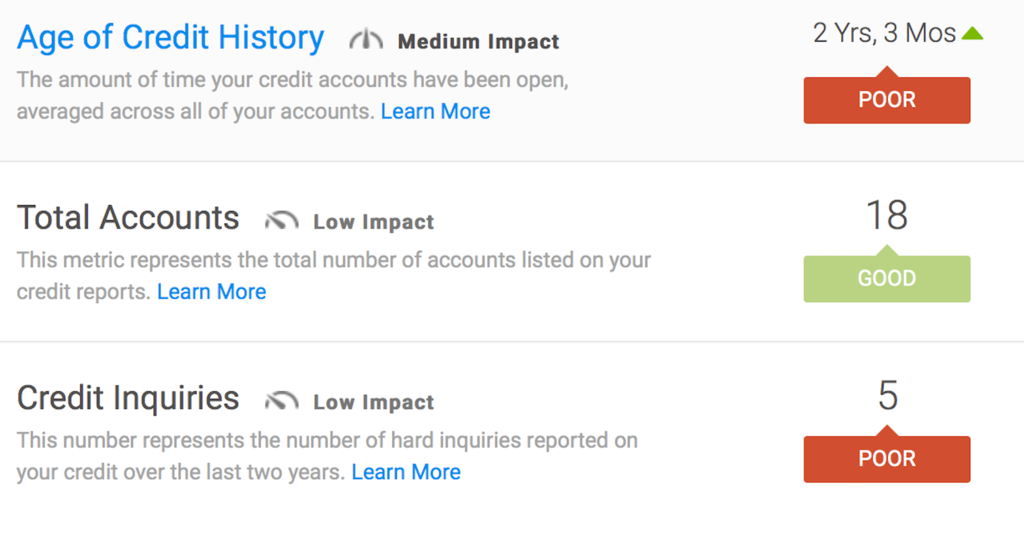

Total revolving limits 741200 (620700 reporting) FICO 8: EQ 703 TU 704 EX 691

Message 17 of 18

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

08-23-2015

08:32 AM

08-23-2015

08:32 AM

Re: Refinance or Balance Transfer ?

@SouthJamaica wrote:

@Anonymous wrote:

@kdm31091 wrote:I'd lean towards refinancing the loan vs putting it on a credit card. Your utilization will skyrocket, which is going to lower your score. While this is temporary (as temporary as the high util, anyway), if you're just starting out, tanking your scores may not make you feel so great. There is no compelling advantage that I see to putting it on a credit card.

the whole point of doing this was so i can be ready to sell the car at anytime. It's a 2005 vehicle. I could just give it to CarMax with a lien but i thought if I will have the title to the car that would give me negotiation power. Also if i decide to keep the car... the car insurance would be much cheaper costing me $50 a month instead of $115 i am paying now reqired by WellsFargo. Will no longer be required to have full coverage after Wells Fargo releases the lien to me.

Once i sold the car i go back and pay off the credit card i transferred the balance to. Though i would hate to put a tent on my credit even if its temporary as others have stated would not make me feel good at all. I don't think $5,000 would put much harm though. $10,000 would especially if i do not get a sufficient limit. They would have to give me $100,000 limit just to be at 10% utilization. I also like to make the most of my hard inquiries. So if i apply for Chase Slate i would apply for Chase Sapphire (2 cards for 1 inquiry). I also wanted the US Bank Cash+recent offers sitting on the table ...18 months 0% cash rewards from WellsFargo$150 cash back Blue Cash American Express. 0% 15 months$250 cash back American Express Everyday (white card).and 100,000 points bonus American Express Platinum.Pennsylvania State Employeees Credit Union i hear to combine visa transfer card and Personal Line of Credit in which if i do not use my credit cards a PLOC will not close due to inactivity which may be good to keep my credit score from dropping (doormat) if i never use credit cards living abroad for a couple of years ? anything know about this ? Then maybe thats where i should maybe invest my hard inquires getting a PLOC instead

With Who? Carmax don't negotiate!

and regardless don't see how a title helps with negotiating a selling price.

Message 18 of 18

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.