- myFICO® Forums

- Types of Credit

- Credit Cards

- Why so many cards?

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Why so many cards?

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:45 PM

03-20-2013

11:45 PM

Re: Why so many cards?

@distantarray wrote:

@HiLine wrote:I am specifically asking about FICO scores. How lenders view your credit profile otherwise is irrelevant ...

Remember Fico scores are irrelevant if the banks don't like your credit profile.

Totally. I'm only concerned about FICO scores in this instance though, since thom02099 claimed that having many cards helped him reach an 800 score faster than having few cards would.

Message 51 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:49 PM

03-20-2013

11:49 PM

Re: Why so many cards?

@Dustink wrote:

@HiLine wrote:But as far as payment history goes, FICO only cares about AAoA, timeliness of payments, and the length of credit history, correct? Having more credit cards doesn't help any of these factors. I must be missing something...

Why does the FICO matter?

having more credit cards will prove to the under writters that your responsible and capable of managing multiple lines. Kind of like how a waitress who can juggle more tables and stay professional is usually considered more valuable. Regardless after so many manual reviews of your credit by underwritters can ding you for having excessive amount of credit lines open. Cause it could pose a risk of credit pyramiding where you rob one to pay another. Or where you can prepare to max out your credit cards and file bankruptcy isn't unheard of.

total credit limits $108,400 Credit scores Ex 728 EQ 738 TU 758

Message 52 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:51 PM

03-20-2013

11:51 PM

Re: Why so many cards?

@Dustink wrote:

@HiLine wrote:

@Dustink wrote:

@HiLine wrote:

@Dustink wrote:Most of the categories slip it in in some sense. Mix of accounts being the most obvious (not enough accounts to have a mix), payment history next (lack of or good history). I feel it mainly comes down to a lenders criteria. An applicant may have 1 credit card and a FICO of 720, then get declined for insufficient revolving history.

I always thought you'd need a different type of credit such as a personal loan or auto loan to improve the mix of accounts, no? Does having more cards actually help payment history even if you never miss a payment?

Sometimes auto loans and personal loans actually bring down a score, which makes sense from a risk perspective. You are tide down to a payment, thus less $$$ is available for other debts.

Generally, a few credit cards will yield a nice score. A mortgage in time will add positively to the mix. Which also from a risk perspective makes sense, it shows you are consistent and reliable enough to sustain a large payment on a high dollar asset.

Yes, more cards does help payment history. distant's 3-1 card example was perfect. The more cards you have, the more payments you are making. Look at it this way, you have 1 card for 10 years. That is 120 payments. If you instead had a 100 cards, that would be 12,000 payments. That would for sure bump a FICO for payment history.

But as far as payment history goes, FICO only cares about AAoA, timeliness of payments, and the length of credit history, correct? Having more credit cards doesn't help any of these factors. I must be missing something...

Why does the FICO matter?

I can leave this question to others to answer. My only question is why having many credit cards helps your FICO score. Not why having many credit cards helps your credit profile.

Message 53 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:52 PM

03-20-2013

11:52 PM

Re: Why so many cards?

@HiLine wrote:

@Dustink wrote:

@HiLine wrote:

@Dustink wrote:Most of the categories slip it in in some sense. Mix of accounts being the most obvious (not enough accounts to have a mix), payment history next (lack of or good history). I feel it mainly comes down to a lenders criteria. An applicant may have 1 credit card and a FICO of 720, then get declined for insufficient revolving history.

I always thought you'd need a different type of credit such as a personal loan or auto loan to improve the mix of accounts, no? Does having more cards actually help payment history even if you never miss a payment?

Sometimes auto loans and personal loans actually bring down a score, which makes sense from a risk perspective. You are tide down to a payment, thus less $$$ is available for other debts.

Generally, a few credit cards will yield a nice score. A mortgage in time will add positively to the mix. Which also from a risk perspective makes sense, it shows you are consistent and reliable enough to sustain a large payment on a high dollar asset.

Yes, more cards does help payment history. distant's 3-1 card example was perfect. The more cards you have, the more payments you are making. Look at it this way, you have 1 card for 10 years. That is 120 payments. If you instead had a 100 cards, that would be 12,000 payments. That would for sure bump a FICO for payment history.

But as far as payment history goes, FICO only cares about AAoA,

timeliness of payments, and the length of credit history, correct? Having more credit cards doesn't help any of these factors. I must be missing something...

That is why somebody with only 1 card could have a high fico. It does not have a category for number of accounts. This needs to be assessed by a lender, because the right number will vary for everyone.

It comes down to a lenders choice.

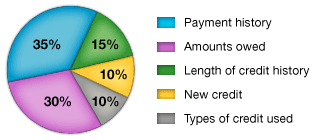

Though, the FICO for a person with only 1 card will be impacted by the things I mentioned before. It is not timeliness of it payments, it is payment history. Payment history comprises about 35% of the score. They can make that mean a lot of things. It is not simply all payments have been made +300, it is a secret formula that we shall not know.

Too many INQs & low AAoA so I'm off to tend the Garden. Age:23

$17k $8.5K Closed $19k $6.5k $24.2k Closed $5k Closed $8.5k Closed @2.49%

$17k $8.5K Closed $19k $6.5k $24.2k Closed $5k Closed $8.5k Closed @2.49%

Message 54 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:54 PM

03-20-2013

11:54 PM

Re: Why so many cards?

@HiLine wrote:

@Dustink wrote:

@HiLine wrote:

@Dustink wrote:

@HiLine wrote:

@Dustink wrote:Most of the categories slip it in in some sense. Mix of accounts being the most obvious (not enough accounts to have a mix), payment history next (lack of or good history). I feel it mainly comes down to a lenders criteria. An applicant may have 1 credit card and a FICO of 720, then get declined for insufficient revolving history.

I always thought you'd need a different type of credit such as a personal loan or auto loan to improve the mix of accounts, no? Does having more cards actually help payment history even if you never miss a payment?

Sometimes auto loans and personal loans actually bring down a score, which makes sense from a risk perspective. You are tide down to a payment, thus less $$$ is available for other debts.

Generally, a few credit cards will yield a nice score. A mortgage in time will add positively to the mix. Which also from a risk perspective makes sense, it shows you are consistent and reliable enough to sustain a large payment on a high dollar asset.

Yes, more cards does help payment history. distant's 3-1 card example was perfect. The more cards you have, the more payments you are making. Look at it this way, you have 1 card for 10 years. That is 120 payments. If you instead had a 100 cards, that would be 12,000 payments. That would for sure bump a FICO for payment history.

But as far as payment history goes, FICO only cares about AAoA, timeliness of payments, and the length of credit history, correct? Having more credit cards doesn't help any of these factors. I must be missing something...

Why does the FICO matter?

I can leave this question to others to answer. My only question is why having many credit cards helps your FICO score. Not why having many credit cards helps your credit profile.

For most people when they have add an additional card, their total CL will increase (since no card has a CL = 0). All other things equal, a larger CL will equate to a lower util% at any given time, which increases FICO.

If I spend an average of 5k per month and I have 10k in total lines, my util is 50%. Now if I add another card and I have 15k in total credit lines, my util drops to 33% and my score improves.

EX 798, EQ 789, TU 784

American Express Platinum (NPSL) || Bank of America Privileges with Travel Rewards Visa Signature - $23,200 CL

Barclays American Airlines Aviator Red World Elite Mastercard - $20,000 CL || Chase IHG Rewards World Mastercard - $25,000 CL

Chase Sapphire Preferred Visa Signature - $12,700 CL || Chase United MileagePlus Club World Elite MasterCard - $26,500 CL

Citibank Hilton Reserve Visa Signature - $20,000 CL || J.P. Morgan Ritz Carlton Visa Signature - $23,500 CL

American Express Platinum (NPSL) || Bank of America Privileges with Travel Rewards Visa Signature - $23,200 CL

Barclays American Airlines Aviator Red World Elite Mastercard - $20,000 CL || Chase IHG Rewards World Mastercard - $25,000 CL

Chase Sapphire Preferred Visa Signature - $12,700 CL || Chase United MileagePlus Club World Elite MasterCard - $26,500 CL

Citibank Hilton Reserve Visa Signature - $20,000 CL || J.P. Morgan Ritz Carlton Visa Signature - $23,500 CL

Message 55 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:54 PM

03-20-2013

11:54 PM

Re: Why so many cards?

@HiLine wrote:

@distantarray wrote:

@HiLine wrote:I am specifically asking about FICO scores. How lenders view your credit profile otherwise is irrelevant ...

Remember Fico scores are irrelevant if the banks don't like your credit profile.

Totally. I'm only concerned about FICO scores in this instance though, since thom02099 claimed that having many cards helped him reach an 800 score faster than having few cards would.

1. 800 score does nothing but look nice in your head

2. after 720 majority of banks consider that A+ and a few banks will consider 760+ Prime but that just means you should take your business elsewhere imo.

If you want to increase your score that bad FAST! get as many authorized user accounts from responsible people with a good credit history.

Even the Fico president encourages it http://www.youtube.com/watch?v=4SsgjAwZ_ZE

It's basically a copy and paste of their credit history onto yours, you can get 60 years of credit history (about maximum since credit cards have only been around that long lol) if they add you to their card.

total credit limits $108,400 Credit scores Ex 728 EQ 738 TU 758

Message 56 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:55 PM

03-20-2013

11:55 PM

Re: Why so many cards?

@HiLine wrote:

@distantarray wrote:

@HiLine wrote:I am specifically asking about FICO scores. How lenders view your credit profile otherwise is irrelevant ...

Remember Fico scores are irrelevant if the banks don't like your credit profile.

Totally. I'm only concerned about FICO scores in this instance though, since thom02099 claimed that having many cards helped him reach an 800 score faster than having few cards would.

FICO is a risk assessment. In some way the scoring model is able to see that somebody managing more accounts is less risky. Likely fit into the payment history category.

Too many INQs & low AAoA so I'm off to tend the Garden. Age:23

$17k $8.5K Closed $19k $6.5k $24.2k Closed $5k Closed $8.5k Closed @2.49%

$17k $8.5K Closed $19k $6.5k $24.2k Closed $5k Closed $8.5k Closed @2.49%

Message 57 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-20-2013

11:59 PM

03-20-2013

11:59 PM

Re: Why so many cards?

@HiLine wrote:

I can leave this question to others to answer. My only question is why having many credit cards helps your FICO score. Not why having many credit cards helps your credit profile.

Ok in theory after 2-3 cards it won't help at all if you open up 2-3 cards at once, and you NEVER apply for anything else ever again.

Does having more credit cards help you get faster into 800? In majority of the Cases yes.

Cause majority of people WILL apply for new loans, or credit cards along the way. The most important factor that usually keeps consumers out of the 800 club is Average age of accounts.

Now let's say I have 10 credit cards openned today. and you have 2.

5 years down the line I apply for 1 more card or loan. My average age of accounts goes from 5 years to 4.5 years.

If you have 2 and apply for one 5 years down the line you'll go from 5 year to only 1.66 years average.

usually average age of accounts of 10+ years are required. If you see the video http://www.youtube.com/watch?v=4SsgjAwZ_ZE

The fico president states you usually have to be in the 40's to get a close to perfect score.

total credit limits $108,400 Credit scores Ex 728 EQ 738 TU 758

Message 58 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-21-2013

12:00 AM

03-21-2013

12:00 AM

Re: Why so many cards?

@distantarray wrote:

@Dustink wrote:

@HiLine wrote:But as far as payment history goes, FICO only cares about AAoA, timeliness of payments, and the length of credit history, correct? Having more credit cards doesn't help any of these factors. I must be missing something...

Why does the FICO matter?

having more credit cards will prove to the under writters that your responsible and capable of managing multiple lines. Kind of like how a waitress who can juggle more tables and stay professional is usually considered more valuable. Regardless after so many manual reviews of your credit by underwritters can ding you for having excessive amount of credit lines open. Cause it could pose a risk of credit pyramiding where you rob one to pay another. Or where you can prepare to max out your credit cards and file bankruptcy isn't unheard of.

Awesome! Thanks for the chart! Now my question is which of those 5 factors having many credit cards possibly helps. I guess payment history? So I looked here: http://www.myfico.com/CreditEducation/Credit-Payment-History.aspx

Quote:

"A good track record on most of your credit accounts will increase your FICO® Score."

If I have a good track record on 100% of my credit accounts, does the number of accounts affect this?

Message 59 of 69

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-21-2013

12:05 AM

03-21-2013

12:05 AM

Re: Why so many cards?

@HiLine wrote:

@distantarray wrote:

@Dustink wrote:

@HiLine wrote:But as far as payment history goes, FICO only cares about AAoA, timeliness of payments, and the length of credit history, correct? Having more credit cards doesn't help any of these factors. I must be missing something...

Quote:

"A good track record on most of your credit accounts will increase your FICO® Score."

If I have a good track record on 100% of my credit accounts, does the number of accounts affect this?

Number of accounts and when they were openned will have an affect on your average age of accounts. Which is 15% of your score.

So technically if you openned all the accounts at once it won't make a difference, but applied for things at different dates and time will skew the average age which will alter your credit score.

If you don't have multiple lines then your average age will suffer greatly when you open a new account. 10 year average on 1 account, will shrink to a mere 5 after 1 new card, and 3.33 years if you add 2.

If you have 10 accounts for 10 years, then adding one would only go from 10 years average to about 9 and another to 8.33.

Having more account just protects your average account age. So if your planning to apply for cards occassionally keeping more accounts open could help.

Personally AAOA is something I could care very little about. I've given up the 800 score dream. Even with a terrible AAOA I can maintain a 720-760 without a problem as long as I keep my balances down. Since applying for new cards gets me 100% free vacations every year ![]()

800 score bragging rights to random strangers online who cares about the score? < Free Vacations that makes me happy, and friends jealous who don't care about credit scores ![]()

total credit limits $108,400 Credit scores Ex 728 EQ 738 TU 758

Message 60 of 69

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.