- myFICO® Forums

- Bouncing Back from Credit Problems

- Rebuilding Your Credit

- Can I break 700?

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Can I break 700?

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-05-2014

08:30 AM

05-05-2014

08:30 AM

Can I break 700?

Pretty simple question, and I can probably answer my own question by saying this is based case by case. But I was wondering if anyone has a 700+ score with a charged off account reporting?

I have a charged off account that is reporting from 2011 and haven't gotten anywhere with Discover.

On a different note, I'd like to thank everyone for their help. I've managed to raise my score from 592 TU to 685 TU in just over 2 months time. I say 90+ points is a success! I'd like to get over a 700, But not sure what steps to take to gain that 15 points.

Will adding a mortgage to my CR bump my score up after some time? I'm sure initially it will go down, but wondering if a mortgage has any more impact on your CR than adding a new CC? I was pre-approved for a mortage with a mid-score of 636 2 months ago (592 TU was my low score), but wanted to clean up my reports to get a better rate, that's when my mission started. I'll be applying for a mortgage in August with a now cleanER report. Thanks again for all of your help!

Message 1 of 10

0

Kudos

9 REPLIES 9

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-05-2014

03:41 PM

05-05-2014

03:41 PM

Re: Can I break 700?

@bigB12 wrote:Pretty simple question, and I can probably answer my own question by saying this is based case by case. But I was wondering if anyone has a 700+ score with a charged off account reporting?

I have a charged off account that is reporting from 2011 and haven't gotten anywhere with Discover.

On a different note, I'd like to thank everyone for their help. I've managed to raise my score from 592 TU to 685 TU in just over 2 months time. I say 90+ points is a success! I'd like to get over a 700, But not sure what steps to take to gain that 15 points.

Will adding a mortgage to my CR bump my score up after some time? I'm sure initially it will go down, but wondering if a mortgage has any more impact on your CR than adding a new CC? I was pre-approved for a mortage with a mid-score of 636 2 months ago (592 TU was my low score), but wanted to clean up my reports to get a better rate, that's when my mission started. I'll be applying for a mortgage in August with a now cleanER report. Thanks again for all of your help!

Sure you can break 700 with a CO as the baddies age and good TL's gain history the CO has less of a scoring factor..

Case in point I had a old FED tax lien at one point and a CO and was in the 700's

Before you app think...

Have you done your research of the CC?

Does it fit your spending?

Do you have a plan for the bonus w/o going into debt?

Can you afford the AF?

Do you know the cards benefits? Is it worth the HP?

Have you done your research of the CC?

Does it fit your spending?

Do you have a plan for the bonus w/o going into debt?

Can you afford the AF?

Do you know the cards benefits? Is it worth the HP?

Message 2 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-05-2014

04:08 PM

05-05-2014

04:08 PM

Re: Can I break 700?

Yes, as MJ has already stated as they age their impact is less and less on your score so you can have 700+ with COs.

Message 3 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-05-2014

04:32 PM

05-05-2014

04:32 PM

Re: Can I break 700?

bigB12 wrote:

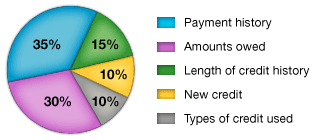

Will adding a mortgage to my CR bump my score up after some time? I'm sure initially it will go down, but wondering if a mortgage has any more impact on your CR than adding a new CC?

Good question

Here's what goes into Fico scoring

So adding any of the above categories if you don't have can certainly have a positive impact on scores

However a new TL can equal +/- depending on other key factors of your CR's

Some have seen a mortgage report and increase scores while others take a scoring hit

Before you app think...

Have you done your research of the CC?

Does it fit your spending?

Do you have a plan for the bonus w/o going into debt?

Can you afford the AF?

Do you know the cards benefits? Is it worth the HP?

Have you done your research of the CC?

Does it fit your spending?

Do you have a plan for the bonus w/o going into debt?

Can you afford the AF?

Do you know the cards benefits? Is it worth the HP?

Message 4 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-05-2014

09:56 PM

05-05-2014

09:56 PM

Re: Can I break 700?

I would say that the fact that while adding a mortgage could initially have either positive or NEGATIVE effect, it definitively will help you over time. A mortgage is rated as the highest quality of credit, followed by installment loans, then credit cards. It definitely is a big plus to get a mortgage in your mix. :-)

Starting Score: TU 490 on 11/2012

Starting Score: TU 490 on 11/2012Current Score:6/16/15:EQ 714, EX 704, TU 702 (all from myFICO)

New Goal Score: 740+ for all three

Message 5 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2014

03:48 AM

05-06-2014

03:48 AM

Re: Can I break 700?

I'm on the verge of 700 right now, and that is with a high balance reporting in April...I have an old BK and a 2 year old CO on my report....so yeah, you can get there.

(EX08 - 654) --- (TU08 - 643) --- (EQ08 - 667) --- (EQ04 - 676)

Message 6 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2014

03:59 AM

05-06-2014

03:59 AM

Re: Can I break 700?

I have a Chase account that was charged off in 2009. I have asked Chase for Goodwill a few times and even recently got a letter back from EO stating that they "respectfully declined my request to remove the reporting". Oh well. I am not applying for a mortgage or anything, so it isn't really urgent for me to get it removed.

Amex ED $19.5k - BoA Travel Rewards $15k - CSP $5k - SDFCU EMV $15k - NFCU goRewards $20k - Barclays Arrival $6.5k

Message 7 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2014

10:40 AM

05-06-2014

10:40 AM

Re: Can I break 700?

Yes, 686 here on EQ, with a major derog from 2011. When this hits the three year mark, it may give another little bump. Right now, it's all about utilization. Recently got a 9pt bump for paying down 1%.

Message 8 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2014

02:50 PM

05-06-2014

02:50 PM

Re: Can I break 700?

Thanks for all of your notes. I'll keep you all updated with how my mortgage app goes.

Message 9 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-06-2014

03:08 PM

05-06-2014

03:08 PM

Re: Can I break 700?

I just pulled my credit reports on MyFico and I have a 713 experian credit score with Midland still reporting as a negative. Equifax is reporting 653 and Transunion 651. Only difference between all three is that experian dosnt show a current balance while the other two do. Hope this helps.

Scores as of 05.14.14

Experian: 713 Equifax: 653 TransUnion: 734

Experian: 713 Equifax: 653 TransUnion: 734

Message 10 of 10

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.