- myFICO® Forums

- Bouncing Back from Credit Problems

- Rebuilding Your Credit

- To Dispute or Not to Dispute...

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

To Dispute or Not to Dispute...

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-31-2012

06:18 PM

01-31-2012

06:18 PM

To Dispute or Not to Dispute...

I started rebuilding my credit score a little while back, while it has raised, it isn't where I'd like it to be. I recently purchased a new vehicle, and while I got a great finance rate, I did not qualify for the 0% financing. The finance guy at the dealership told me that I should go through my report and dispute any negative information, wait 6 months or so, and refinance the vehicle and I should qualify for an even lower rate. I pulled up my credit report and I came across a few questions, and figured this would be my best source for some help.

1) I have an old account that is listed as a "neutral" I guess it would be called? It says "Current Status Unknown." It was a credit card that was opened in 2003. It went to collections, and was paid in full to the collector. In the "Type" field it says "Transferred to another lender or purchaser." ---- My question: Should I dispute this from my report? Is it leaving a negative mark on my credit? Or is the fact that it is my oldest account a good thing to keep on my report?

2) I have 3 collections listed on my report. The accounts all show "Current Closed" for their status. The "Type" does refer to them being collection accounts. ---- My questions: Although the accounts say "Current Closed," do they still report as negative for the previous late payments?

Other than the "Neutral" account and the 3 "Current Closed" accounts, I have 3 "Current Open" accounts (2 credit, 1 vehicle loan) which have never been late. I can only assume that either the "Neutral" account that says it was bought out by a collector, or the 3 "Current Closed" accounts under collectors are attributing to the negative reporting on my score. Should I dispute all of them to have them removed? Also, if I do dispute them, do I dispute through the actual company, or through each credit bureau? (The Neutral account has no contact information whatsoever listed- no phone, no address.)

Thank you so much in advance for your help!

Message 1 of 4

0

Kudos

3 REPLIES 3

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-31-2012

06:29 PM

01-31-2012

06:29 PM

Re: To Dispute or Not to Dispute...

1) What is the DOFD on the OC account? The collection will expire of its own old age after 7 years plus 180 days from the DOFD on the OC account, so you need to know when it will be excluded should you do nothing. Assertions of incorrect status are usually due to a misunderstanding by the consumer as to what was actually reported, and how it impacts their actual status codes. Regardless, the remedy for inaccuracies is not required deletion of the information. They merely have to correct it to overcome any inaccuracies.

YOu would not dispute the "account," just the specfic inaccuracy that you assert.

2) When you refer to "accounts," what specifically are you referencing? A collection "account" is totally separate from an OC account. They are reported to the CRAs as collections, yet quite often commercial credit reports jumble information in a manner that confuses the actual source of who reported, and what was reported. All collections, once paid, have a status of "closed." The prior late payments were not reported by the debt collector, they were reported by the OC. Correction of the collection status, if incorrect, once again wont require deletion of anythng, and wont relate to any prior reporting of OC account delinquencies.

Message 2 of 4

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

01-31-2012

07:01 PM

01-31-2012

07:01 PM

Re: To Dispute or Not to Dispute...

You'll have to forgive me, I'm still learning my credit lingo, but I think I got what you're saying

1) The DOFD for the OC is Sept 2004. This is very close to the 7 years + 180 days. Will I need to take any action once it has reached that point?

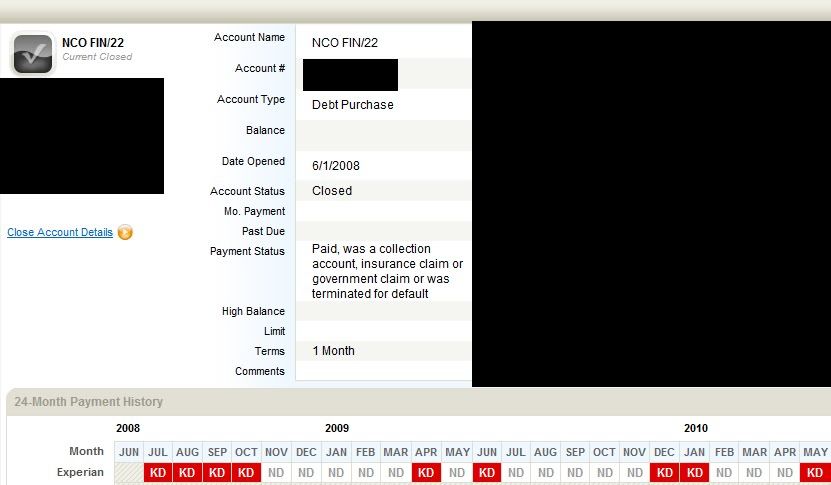

2) These are actual collection accounts. The OC's are not on my credit report. One is listed as "Collection Department/ Agency/ Attorney" and the other two as "Debt Purchase." I attached a picture of a portion of my Experian report which shows how it is reporting. I don't know a lot about these, but I know that red is bad in this case. Also- this was paid in full, not defaulted on.

Thank you again for the help- I really appreciate it.

Message 3 of 4

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-01-2012

12:45 AM

02-01-2012

12:45 AM

Re: To Dispute or Not to Dispute...

Its a paid, closed collection. The source of the collection is immaterial to its required exclusion from your CR. I see nothing to dispute.

If the DOFD on the OC account is 9/2004, it must cease to be included in your CR after 3/2012. Period.

The status or any other reporting is immaterial to the required exclusion of the collection from your CR after that date.

No, you dont have to do anything. The CRAs are required to monitor the DOFD on all collections, and are barred under the statute from continued inclusion of the collection in your CR after its exclusion date.

Let us know if they fail to exlcude after that date, and we will give you the procedure to follow.

Message 4 of 4

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.