- myFICO® Forums

- Types of Credit

- Credit Cards

- Re: My score drop 14 points

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

My score drop 14 points

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

09-30-2012

08:14 PM

09-30-2012

08:14 PM

Re: My score drop 14 points

@LionLaw wrote:If you pay your card with the $400 limit down to zero (and don't increase the balance on your other card), you'll get a nice boost for:

--Reducing your overal util%

--No longer having a card that's close to maxed out

--Having a zero balance on one of your cards.

If that balance going from 0 to $300 was the only thing that changed when your score dropped 14 points, then paying it back to zero will probably get you back all of those points.

agree

| Current: Fico ScoresEQ~706 TU~719 EX 709 4/28/23 Inquiries (24 Months): EQ 0 TU 0 EX 0| Most Recent: A LONG WHILE | Buy A Home Earn Cash Back | Amex Zync(Unicorn) Chase Freedom$1500 Discover IT$7,400 Citi DC $10,000 Citizens Mastercard$7,000 |

Message 11 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

09-30-2012

08:57 PM

09-30-2012

08:57 PM

Re: My score drop 14 points

@afjock21 wrote:

@nicholasyud wrote:So i let one of my card went to 300 dollars balance within 400 limit but i do have other card with 1300 limit total everything.....my total balacen around 250/1300 /////my score drop down 14 points ? wouuld anyone explain please ?

From what I understand your utilization is MOST of you score... I mean, doesn't it make sense?? Geez.... wouldn't it be nice if the HIGHER UTIL meant higher score hahaha

Utilization is 30% of your FICO score. That is a big chunk, but it is not most.

Message 12 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

09-30-2012

08:58 PM

09-30-2012

08:58 PM

Re: My score drop 14 points

i just tryna test out the system.......well i probably paid it off soon but the thing is the bill is not going to report until the end of the month...so.......i might not know my score until next month but will keep you all update.........didnt know about 20% out of 26% over all utili would drop my score that much since i paid everything in full.....

Starting Score: 560

Starting Score: 560Current Score: ?

Goal Score: 800

Message 13 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

09-30-2012

09:05 PM

09-30-2012

09:05 PM

Re: My score drop 14 points

straight form myfico

| Current: Fico ScoresEQ~706 TU~719 EX 709 4/28/23 Inquiries (24 Months): EQ 0 TU 0 EX 0| Most Recent: A LONG WHILE | Buy A Home Earn Cash Back | Amex Zync(Unicorn) Chase Freedom$1500 Discover IT$7,400 Citi DC $10,000 Citizens Mastercard$7,000 |

Message 14 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

09-30-2012

09:08 PM

09-30-2012

09:08 PM

Re: My score drop 14 points

i mean 26% utili from 1% last months ? 14 points ? is that seem like a lot to you all ?

Starting Score: 560Current Score: ?

Goal Score: 800

Message 15 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-07-2012

03:09 AM

10-07-2012

03:09 AM

Re: My score drop 14 points

Fico weird I swear....score bump back up 660 today and don't known why ????

i remove my name as authorite user on the new discover card 2 days ago........are they updated that quick ???

.the score drop 14 point when my 300/400 limit report on sep 30

and after a week today oct 7 went back to 660......hmmmmmmmmmm......

Starting Score: 560Current Score: ?

Goal Score: 800

Message 16 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-07-2012

03:18 AM

10-07-2012

03:18 AM

Re: My score drop 14 points

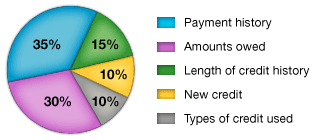

so, where does utilization come in play on the pie chart?

FICO EQ: 633 8/15/12

lender pulled 11/3/12 EQ 661 TU 650 EX598

credit Karma 674 credit sesame: 663

B/K discharged 2/2006......closed 8/2012

May your limits be high and your balances low!

lender pulled 11/3/12 EQ 661 TU 650 EX598

credit Karma 674 credit sesame: 663

B/K discharged 2/2006......closed 8/2012

May your limits be high and your balances low!

Message 17 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-07-2012

04:02 AM

10-07-2012

04:02 AM

Re: My score drop 14 points

The amounts owed 30% .

TU 746 (10/13)

GOAL: 750+

GOAL: 750+

Message 18 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-07-2012

05:00 AM

10-07-2012

05:00 AM

Re: My score drop 14 points

@nicholasyud wrote:Fico weird I swear....score bump back up 660 today and don't known why ????

i remove my name as authorite user on the new discover card 2 days ago........are they updated that quick ???

.the score drop 14 point when my 300/400 limit report on sep 30

and after a week today oct 7 went back to 660......hmmmmmmmmmm......

sw has been known to do some weird things.

i was i dropped to 692 one day then next day went up to 708 then 710 then dropped to 682 now all in the span of like 5 days. (well the last one is because my auto loan finally reported.

| Current: Fico ScoresEQ~706 TU~719 EX 709 4/28/23 Inquiries (24 Months): EQ 0 TU 0 EX 0| Most Recent: A LONG WHILE | Buy A Home Earn Cash Back | Amex Zync(Unicorn) Chase Freedom$1500 Discover IT$7,400 Citi DC $10,000 Citizens Mastercard$7,000 |

Message 19 of 23

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-07-2012

10:38 AM

10-07-2012

10:38 AM

Re: My score drop 14 points

any experts in da house ?

Starting Score: 560Current Score: ?

Goal Score: 800

Message 20 of 23

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.