- myFICO® Forums

- FICO Scoring and Other Credit Topics

- Understanding FICO® Scoring

- Re: paying down 10 G's of debt!!!

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

paying down 10 G's of debt!!!

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-16-2007

08:58 PM

10-16-2007

08:58 PM

paying down 10 G's of debt!!!

Hi,

I am new! I was curious to see what effect my score will have. I just paid down 10,000 to 4 diff revolving accounts. I paid off one completely...2600. Cut 3 more from 4000 to 1500, 3700 to 1200 and 4900 to 2200! My scores are EX 584 EQ 514 and TU 626....Yuck! In Feb they were all in the high 600's but we maxed out a couple due to home improvement! We still have 12,000 in rev debt. 46,000 in car and installment loans. I need a quick boost in score to refi house....for more home improvement! What effect do you all think this will have????

Message 1 of 10

0

Kudos

9 REPLIES 9

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

07:23 AM

10-17-2007

07:23 AM

Re: paying down 10 G's of debt!!!

Scoring is more about utilization than the $ amount.

Total balance/ CL = Total UTL

individual Bal/ CL - Ind UTL

For score boost makes sure everything is below 50% UTL on individual trade lines. Total UTL under 30% is better and less than 1-9% is ideal.

You may also need to limit the number of cards reporting a balance.

This is different than saving $ -where paying the highest interest rate first.

Total balance/ CL = Total UTL

individual Bal/ CL - Ind UTL

For score boost makes sure everything is below 50% UTL on individual trade lines. Total UTL under 30% is better and less than 1-9% is ideal.

You may also need to limit the number of cards reporting a balance.

This is different than saving $ -where paying the highest interest rate first.

Message 2 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

09:06 AM

10-17-2007

09:06 AM

Re: paying down 10 G's of debt!!!

Hey, Red! Welcome to the insanity!

My only question is.. why are you concerned with your current FICO? If you are not seeking immediate credit, then FICO is just a wet dream that fades upon awakening. It quickly becomes nothing more than crust on the vacated sheets. Eliminating debt and interest payments is not the same strategy as a quick FICO fix. My personal short term goal is simple for me... **bleep** the FICO score, and do what I can to eliminate interest and debt, and thus increase the breadth of my monthly wallet. That is money in my pocket. My current FICO is 717, but it is meaningless, because I am not now actively seeking new credit. A really iimpressive FICO score right now only flatters my ego, and not my id.

If you have six months or a year before you seek new credit, then put your current FICO score in the "been there, done that" manila folder, and concentrate on reducing the monthly outflow of interes $$, That is real money, and not an esoteric FICO that has no meaning today when not seeking immediate credit. Know the game, but dont get sucked into it. Above all other things, improving FICO is a long term game. If you dont need it now, then treat it as an ex-wife.

Message 3 of 10

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

09:47 AM

10-17-2007

09:47 AM

Re: paying down 10 G's of debt!!!

????

RobertEG wrote:

... improving FICO is a long term game. If you dont need it now, then treat it as an ex-wife.

Message 4 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

09:56 AM

10-17-2007

09:56 AM

Re: paying down 10 G's of debt!!!

@Anonymous wrote:????

@RobertEG wrote:... improving FICO is a long term game. If you dont need it now, then treat it as an ex-wife.

I'm still retching over the crusty sheets. Eeeewww...

* Credit is a wonderful servant, but a terrible master. * Who's the boss --you or your credit?

FICO's: EQ 781 - TU 793 - EX 779 (from PSECU) - Done credit hunting; having fun with credit gardening. - EQ 590 on 5/14/2007

FICO's: EQ 781 - TU 793 - EX 779 (from PSECU) - Done credit hunting; having fun with credit gardening. - EQ 590 on 5/14/2007

Message 5 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

10:06 AM

10-17-2007

10:06 AM

Re: paying down 10 G's of debt!!!

I don't have an ex wife

RobertEG wrote:... improving FICO is a long term game. If you dont need it now, then treat it as an ex-wife.

The slide from grace is really more like gliding

And I've found the trick is not to stop the sliding

But to find a graceful way of staying slid

And I've found the trick is not to stop the sliding

But to find a graceful way of staying slid

Message 6 of 10

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

10:10 AM

10-17-2007

10:10 AM

Re: paying down 10 G's of debt!!!

MidnightVoice wrote:

I don't have an ex wife

RobertEG wrote:

... improving FICO is a long term game. If you dont need it now, then treat it as an ex-wife.

Neither do I, and it's guaranteed I never will.

I do have an ex-husband. How should I treat him?

Message 7 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

10:14 AM

10-17-2007

10:14 AM

Re: paying down 10 G's of debt!!!

masdeocho wrote:I do have an ex-husband. How should I treat him?

I don't want to go there.......................................

The slide from grace is really more like gliding

And I've found the trick is not to stop the sliding

But to find a graceful way of staying slid

And I've found the trick is not to stop the sliding

But to find a graceful way of staying slid

Message 8 of 10

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-17-2007

12:53 PM

10-17-2007

12:53 PM

Re: paying down 10 G's of debt!!!

OMG, that is so gross!

@haulingthescoreup wrote:

@Anonymous wrote:????

@RobertEG wrote:... improving FICO is a long term game. If you dont need it now, then treat it as an ex-wife.

I'm still retching over the crusty sheets. Eeeewww...

Message 9 of 10

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

10-18-2007

12:16 PM

10-18-2007

12:16 PM

Re: paying down 10 G's of debt!!!

For your Fico Score to make a difference in your monthly payments for a 30 year fixed rate refinance see chart below.

FICO score APR Monthly payment * 760-850 6.016% $1,501 700-759 6.238% $1,537 660-699 6.522% $1,584 620-659 7.332% $1,719 580-619 9.639% $2,127 500-579 10.625%

$2,310

It looks to me that you seem to have a lot of debt already so I think refinancing your home might be a big mistake. Your main goal right now should be paying off more of the debt and on time so that your score will become between 760 and 850. If you get your score in this range you will get the best rate. The only problem with this is it might take you a few years to accomplish this. You can not change a Fico score overnight, it take lots of time and effort. Below shows you how your Fico score is calculated.

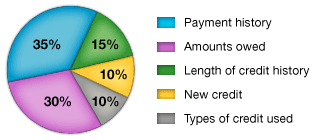

What’s In Your FICO ScoreFICO Scores are calculated from a lot of different credit data in your credit report. This data can be grouped into five categories as outlined below. The percentages in the chart reflect how important each of the categories is in determining your FICO score.

These percentages are based on the importance of the five categories for the general population. For particular groups - for example, people who have not been using credit long - the importance of these categories may be somewhat different.

Payment History- Account payment information on specific types of accounts (credit cards, retail accounts, installment loans, finance company accounts, mortgage, etc.)

- Presence of adverse public records (bankruptcy, judgements, suits, liens, wage attachments, etc.), collection items, and/or delinquency (past due items)

- Severity of delinquency (how long past due)

- Amount past due on delinquent accounts or collection items

- Time since (recency of) past due items (delinquency), adverse public records (if any), or collection items (if any)

- Number of past due items on file

- Number of accounts paid as agreed

- Amount owing on accounts

- Amount owing on specific types of accounts

- Lack of a specific type of balance, in some cases

- Number of accounts with balances

- Proportion of credit lines used (proportion of balances to total credit limits on certain types of revolving accounts)

- Proportion of installment loan amounts still owing (proportion of balance to original loan amount on certain types of installment loans)

- Time since accounts opened

- Time since accounts opened, by specific type of account

- Time since account activity

- Number of recently opened accounts, and proportion of accounts that are recently opened, by type of account

- Number of recent credit inquiries

- Time since recent account opening(s), by type of account

- Time since credit inquiry(s)

- Re-establishment of positive credit history following past payment problems

- Number of (presence, prevalence, and recent information on) various types of accounts (credit cards, retail accounts, installment loans, mortgage, consumer finance accounts, etc.)

Please note that:

- A FICO score takes into consideration all these categories of information, not just one or two.

No one piece of information or factor alone will determine your score. - The importance of any factor depends on the overall information in your credit report.

For some people, a given factor may be more important than for someone else with a different credit history. In addition, as the information in your credit report changes, so does the importance of any factor in determining your FICO score. Thus, it's impossible to say exactly how important any single factor is in determining your score - even the levels of importance shown here are for the general population, and will be different for different credit profiles. What's important is the mix of information, which varies from person to person, and for any one person over time. - Your FICO score only looks at information in your credit report.

However, lenders look at many things when making a credit decision including your income, how long you have worked at your present job and the kind of credit you are requesting. - Your score considers both positive and negative information in your credit report.

Late payments will lower your score, but establishing or re-establishing a good track record of making payments on time will raise your FICO credit score.

Message 10 of 10

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.