- myFICO® Forums

- FICO Scoring and Other Credit Topics

- General Credit Topics

- What the F - - (Score drop)

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

What the F - - (Score drop)

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- « Previous

-

- 1

- 2

- Next »

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-04-2009

10:10 AM

05-04-2009

10:10 AM

Re: What the F - - (Score drop)

FICO doesn't release the specifics because they spend the man hours and money doing the research and developing the formula. If they released the specifics, anyone could then duplicate the formula and sell it cheaper because they have no invested anything.

What would be the incentive to develop an accurate formula if you aren't going to be paid for it?

FICO developed a product that lenders trust and pay for. Doesn't matter if we like it or not.

Lenders aren't made to use FICO scores or even use our credit reports when determining what rate we will get, if we'll be approved, etc.

Here is some information regarding how scores are arrived at.

http://www.myfico.com/CreditEducation/WhatsInYourScore.aspx

Message Edited by sidewinder on 05-04-2009 12:11 PM

Message 11 of 13

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-04-2009

10:15 AM

05-04-2009

10:15 AM

Re: What the F - - (Score drop)

Your frustration is understood and, yes, voiced by many.

There is a general understanding of FICO and what most importantly affects it. However, those are general parameters, not specific as to how they actually formulate each component.

If you maintain no derogs, you can expect to not be re-bucketed much after your oldest account is 19 years and your AAoA (average age of accounts) is 6 or more years. You won't have the "growing pain" type decreases associated with "moving up" the buckets. Your score changes will then mostly be based upon how you utilize your credit, debt loads, and payment history. The higher your score (760 plus) and the older your history, the more stable it becomes.

Have you looked at the various FICO resources. They do attempt to better explain how the process works.

http://www.myfico.com/CreditEducation/WhatsInYourScore.aspx

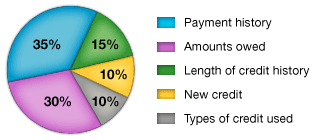

What’s in your FICO® scoreFICO Scores are calculated from a lot of different credit data in your credit report. This data can be grouped into five categories as outlined below. The percentages in the chart reflect how important each of the categories is in determining your FICO score.

These percentages are based on the importance of the five categories for the general population. For particular groups - for example, people who have not been using credit long - the importance of these categories may be somewhat different.

Payment History- Account payment information on specific types of accounts (credit cards, retail accounts, installment loans, finance company accounts, mortgage, etc.)

- Presence of adverse public records (bankruptcy, judgements, suits, liens, wage attachments, etc.), collection items, and/or delinquency (past due items)

- Severity of delinquency (how long past due)

- Amount past due on delinquent accounts or collection items

- Time since (recency of) past due items (delinquency), adverse public records (if any), or collection items (if any)

- Number of past due items on file

- Number of accounts paid as agreed

- Amount owing on accounts

- Amount owing on specific types of accounts

- Lack of a specific type of balance, in some cases

- Number of accounts with balances

- Proportion of credit lines used (proportion of balances to total credit limits on certain types of revolving accounts)

- Proportion of installment loan amounts still owing (proportion of balance to original loan amount on certain types of installment loans)

- Time since accounts opened

- Time since accounts opened, by specific type of account

- Time since account activity

- Number of recently opened accounts, and proportion of accounts that are recently opened, by type of account

- Number of recent credit inquiries

- Time since recent account opening(s), by type of account

- Time since credit inquiry(s)

- Re-establishment of positive credit history following past payment problems

- Number of (presence, prevalence, and recent information on) various types of accounts (credit cards, retail accounts, installment loans, mortgage, consumer finance accounts, etc.)

Please note that:

- A FICO score takes into consideration all these categories of information, not just one or two.

No one piece of information or factor alone will determine your score. - The importance of any factor depends on the overall information in your credit report.

For some people, a given factor may be more important than for someone else with a different credit history. In addition, as the information in your credit report changes, so does the importance of any factor in determining your FICO score. Thus, it's impossible to say exactly how important any single factor is in determining your score - even the levels of importance shown here are for the general population, and will be different for different credit profiles. What's important is the mix of information, which varies from person to person, and for any one person over time. - Your FICO score only looks at information in your credit report.

However, lenders look at many things when making a credit decision including your income, how long you have worked at your present job and the kind of credit you are requesting. - Your score considers both positive and negative information in your credit report.

Late payments will lower your score, but establishing or re-establishing a good track record of making payments on time will raise your FICO credit score.

Message 12 of 13

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-04-2009

05:07 PM

05-04-2009

05:07 PM

Re: What the F - - (Score drop)

Courtesy of Mike14, here is a link with some info on bucketing. It is a heavy read but if you want to really get into the mechanics check this out.

Message 13 of 13

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.