- myFICO® Forums

- FICO Scoring and Other Credit Topics

- Understanding FICO® Scoring

- FICO Scoring and Bankcards

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

FICO Scoring and Bankcards

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-10-2009

08:55 PM

05-10-2009

08:55 PM

FICO Scoring and Bankcards

I keep reading from well known financial columnists is that having a VISA or Mastercard or AMEX will really help your score. The essence behind their statements is they think these types of accounts has more impact on the score than a store departent card. In all of my reading I cannot find any thing to back up these statements that is not just speculation or what some one thinks is true. They are all considered revolving debt and the only difference is the loan type ( charge card and credit card). Anyone have any idea as to where these columnists are getting their information? I have sent several emails but no reply.

Below is a link to one such article in particular the section on get a major credit card

http://articles.moneycentral.msn.com/Banking/YourCreditRating/how-to-win-the-credit-score-game.aspx

Message Edited by AndySoCal on 05-14-2009 07:41 PM

FIC Scores XPN v8 805 V2 831 (SDFCU) TUC V 8 800 07/25 EFX Bankcard v8 822 EFX FIC0 v8 807 Vantage score 4.0 817 via JC Penney

JC Penney 10/2008 4,700 US Bank Cash 08/2010 12,000 Citibank Custom Cash 5/2015 14,100, State Dept. FCU 06/2023 25,000 02/2024 Redstone FCU Signature VISA 10,000 08/23/2024 Commonwealth Credit Union 15000 07/25 Walmart One 5000 12/04/25

Banking: Lafayette FCU Fortera FCU State Department FCU Redstone FCU Hughes FCU Commonwealth FCU

My personal blacklist Axos Bank, Bank of America, Synchrony Bank Capital One TD Bank Comerica Bank BMO US Bank Wells Fargo

JC Penney 10/2008 4,700 US Bank Cash 08/2010 12,000 Citibank Custom Cash 5/2015 14,100, State Dept. FCU 06/2023 25,000 02/2024 Redstone FCU Signature VISA 10,000 08/23/2024 Commonwealth Credit Union 15000 07/25 Walmart One 5000 12/04/25

Banking: Lafayette FCU Fortera FCU State Department FCU Redstone FCU Hughes FCU Commonwealth FCU

My personal blacklist Axos Bank, Bank of America, Synchrony Bank Capital One TD Bank Comerica Bank BMO US Bank Wells Fargo

Message 1 of 5

0

Kudos

4 REPLIES 4

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-11-2009

06:29 PM

05-11-2009

06:29 PM

Re: FICO Scoring and Bankcards

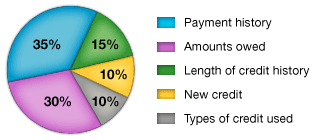

Types of Credit Used

* Number of (presence, prevalence, and recent information on) various types of accounts (credit cards, retail accounts, installment loans, mortgage, consumer finance accounts, etc.)

* Credit is a wonderful servant, but a terrible master. * Who's the boss --you or your credit?

FICO's: EQ 781 - TU 793 - EX 779 (from PSECU) - Done credit hunting; having fun with credit gardening. - EQ 590 on 5/14/2007

FICO's: EQ 781 - TU 793 - EX 779 (from PSECU) - Done credit hunting; having fun with credit gardening. - EQ 590 on 5/14/2007

Message 2 of 5

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-14-2009

07:44 PM

05-14-2009

07:44 PM

Re: FICO Scoring and Bankcards

I updated my original post ot include a link to one such article. The article and others like it is the cause of my original post

FIC Scores XPN v8 805 V2 831 (SDFCU) TUC V 8 800 07/25 EFX Bankcard v8 822 EFX FIC0 v8 807 Vantage score 4.0 817 via JC Penney

JC Penney 10/2008 4,700 US Bank Cash 08/2010 12,000 Citibank Custom Cash 5/2015 14,100, State Dept. FCU 06/2023 25,000 02/2024 Redstone FCU Signature VISA 10,000 08/23/2024 Commonwealth Credit Union 15000 07/25 Walmart One 5000 12/04/25

Banking: Lafayette FCU Fortera FCU State Department FCU Redstone FCU Hughes FCU Commonwealth FCU

My personal blacklist Axos Bank, Bank of America, Synchrony Bank Capital One TD Bank Comerica Bank BMO US Bank Wells Fargo

JC Penney 10/2008 4,700 US Bank Cash 08/2010 12,000 Citibank Custom Cash 5/2015 14,100, State Dept. FCU 06/2023 25,000 02/2024 Redstone FCU Signature VISA 10,000 08/23/2024 Commonwealth Credit Union 15000 07/25 Walmart One 5000 12/04/25

Banking: Lafayette FCU Fortera FCU State Department FCU Redstone FCU Hughes FCU Commonwealth FCU

My personal blacklist Axos Bank, Bank of America, Synchrony Bank Capital One TD Bank Comerica Bank BMO US Bank Wells Fargo

Message 3 of 5

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-14-2009

09:13 PM

05-14-2009

09:13 PM

Re: FICO Scoring and Bankcards

There are numerous articles on this topic that all agree. Major bank cards are more important than dept store cards, for example, and the reason is obvious.

Granting of credit is a risk analysis. Major banks do a much more detailed and rigorous analysis of their card approvals than do small creditors. Most even have their own scoring algorithms that they use in addition to FICO scores. So approval by BOA, or example, means a lot more than approval by Jim's Dept. Store.

Message 4 of 5

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

05-16-2009

10:34 AM

05-16-2009

10:34 AM

Re: FICO Scoring and Bankcards

The FICO hints and comments specifically speak to the need and/or lack of "bankcards."

Message 5 of 5

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.