- myFICO® Forums

- FICO Scoring and Other Credit Topics

- General Credit Topics

- Re: BoA Fico Score (TransUnion)

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

BoA Fico Score (TransUnion)

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-26-2016

08:05 AM

02-26-2016

08:05 AM

BoA Fico Score (TransUnion)

BofA started showing me my TransUnion fico Score. I was just wondering how accurate is this score, is the the fico score I would get here at myfico.com website or is it some other score they generate?

Thanks in advance

")

")

Message 1 of 15

0

Kudos

14 REPLIES 14

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-26-2016

01:27 PM

02-26-2016

01:27 PM

Re: BoA Fico Score (TransUnion)

Sorry I can't help with your question, but I have been waiting to see my TU FICO from BOA. Where do you find it on the website?

TIA!

Message 2 of 15

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-26-2016

01:50 PM

02-26-2016

01:50 PM

Re: BoA Fico Score (TransUnion)

Fico 08, same as Discover, Barclays, CCT, and here at MyFico.

Message 3 of 15

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-26-2016

06:05 PM

02-26-2016

06:05 PM

Re: BoA Fico Score (TransUnion)

@Anonymous wrote:Where do you find it on the website?

TIA!

Yes, where did you find it? I've looked everywhere on the BOA site.

Message 4 of 15

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-26-2016

11:05 PM

02-26-2016

11:05 PM

Re: BoA Fico Score (TransUnion)

Does the OP (SMikulski49) live in Georgia or Pennsylvania? Those two states started receiving their score through BOA several weeks ahead of the other 48 states. The last I heard, the rest of the country was going to get it at the end of March.

Message 5 of 15

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-27-2016

06:04 AM

02-27-2016

06:04 AM

Re: BoA Fico Score (TransUnion)

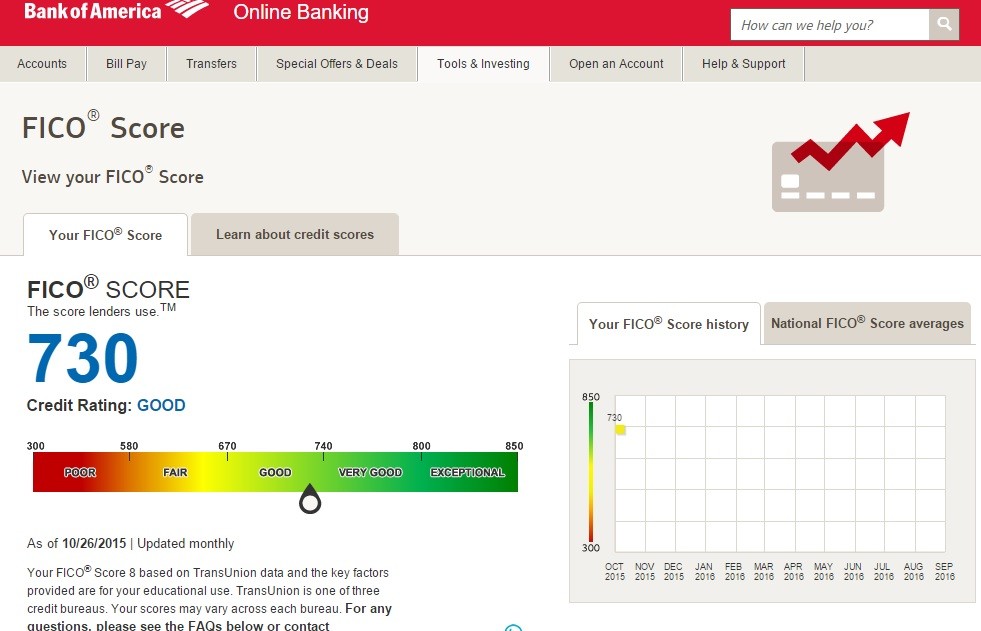

I'm not with BofA but ran across this screenshot. Note the text in the bottom right "Your FICO Score 8 based on TransUnion data". A FICO 8 is a FICO 8 regardless of where you get it from. It's the same scoring model. As long as the data used each time to generate the score didn't change then the numbers generated will be the same.

@SMikulski49 wrote:I was just wondering how accurate is this score

Stop relying on "accuracy" and instead think of relevance. There isn't just one scoring model used by creditors/products. Most use a FICO model. While FICO 8 is the most commonly used model it is not used by all creditors/products. Scores also don't all use the same CRA as a data source. Therefore you need to consider both the model & CRA whenever you reference a score and consider who and what it is relevant to.

If, for example, a creditor uses an EQ FICO 8 Bankcard then a TU FICO 8 (or any other model or CRA) won't be relevant. See also the Understanding FICO Scoring subforum and its stickies for more info on the various FICO models used by creditors. myFICO doesn't provide just one score either. The alerts/updates are FICO 8's but quarterly access is provided to additional models.

Any score is accurate but only for its own model. You cannot use a score generated by one model to determine a score generated by another model or decide on the "accuracy" of a model by comparing it to another. Different models use different algorithms that evaluate report data differently and can even have different score ranges. Don't assume that all models should produce the same numbers.

Message 6 of 15

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-27-2016

04:22 PM

02-27-2016

04:22 PM

Re: BoA Fico Score (TransUnion)

I live in PA maybe that is why I am able to view it. When I log in into my account, I can see a little box to the right where it says check your score, you wont miss it if you can view it. I understand that different modles use different algoriths, I guess I worded my question wrong. I was wonderibg if its a true TransUnion score or some type of a score like creditcarma provides where no lender uses it. But I understand it more now thanks to your good explonation.

Message 7 of 15

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-27-2016

05:07 PM

02-27-2016

05:07 PM

Re: BoA Fico Score (TransUnion)

Well that's the thing buddy. Even the TU score you get from Credit Karma is a true TransUnion score. It is a score that is really drawn on true TransUnion data.

The big idea is that there are these three silos or warehouses for your credit information: TransUnion, Experian, and Equifax. They just hold the information, and the information you have at one might well be a little different from than the information at either of the other two. These three warehouses are called credit bureaus and are also called consumer reporting agencies

Then there are people who make big fancy computer programs that take all that information and spit out a number (often a number between 300 and 850). That number is called a credit score and the computer program is called a computer scoring algorithm (or sometimes a credit scoring model). FICO is a company that makes a ton of these models (and therefore tons of different scores). There's also a company that was created by the three credit bureaus called Vantage and the score they make is called VantageScore. Each credit bureau also makes its own proprietary credit score. There are many other companies that make credit scores.

The big idea though is that a credit scoring algorithm (a computer program) takes data from a credit bureau (a big silo or warehouse) and then spits out a credit score (a number).

When you ask if a score is a true TransUnion score, the answer is that all the credit scores that are drawn on TU data are true TU scores.

But what you may have had in mind was this: is the score that I see at Bank of America one of the scores that FICO makes? And the answer is yes. BOA is using the FICO 8 Classic algorithm. Credit Karma (which you also mention) uses the Vantage Score algorithm. It has the same range as FICO 8 Classic (300-850) but it is made by a different company than FICO.

Hope that helps.

Message 8 of 15

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-27-2016

06:41 PM

02-27-2016

06:41 PM

Re: BoA Fico Score (TransUnion)

Im in GA, but no fico yet on my account with the cashrewards card.

Message 9 of 15

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-27-2016

08:16 PM

02-27-2016

08:16 PM

Re: BoA Fico Score (TransUnion)

I live in GA too and got mine in early January. I had to search for a while to find it. I encourage you to drill down all the different menus. Eventually you should find some link about credit. Or give BOA a call and they will walk you through how to find it.

Message 10 of 15

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.