- myFICO® Forums

- FICO Scoring and Other Credit Topics

- General Credit Topics

- Re: utilization -- pay down or off?

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

utilization -- pay down or off?

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

08:57 AM

03-06-2008

08:57 AM

Re: utilization -- pay down or off?

Right, so, why would the score drop immediately after paying off a loan .... .... .. .

massagemama wrote:It should stay on the report for 10 years after opening the TL.

VistaV wrote:Wouldn't the TL still appear on your report as a paid and closed account, and still offer the benefit of credit history and account variety?

danikasmom wrote:Yes, that is why they don't let people like us run the credit bureaus...we think logically!!! We are dealing with that right now because we are ready to pay off my hubby's truck but don't want his score to drop. Isn't it ridiculous???

Message 11 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

10:16 AM

03-06-2008

10:16 AM

Re: utilization -- pay down or off?

The score would drop because even though your payment history will be reflected on your report from 7-10 years, the account will not have recent "on-time" payments made to it and the account will reflect as paid in full and closed. Doesn't make a whole lot of sense I know, but that is how it works.

Message 12 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

10:26 AM

03-06-2008

10:26 AM

Re: utilization -- pay down or off?

9% Interest is A LOT for a $24K loan. In my opinion I would pay it off. Yes you might have a short drop in your score, but who cares, at that interest rate you are paying about $180 a month in Interest.

Type in your search engine "Loan Amortization Chart" and put in the car note amount your monthly payment and interest. I did it for you, but I can't post the table. It basically says of that $414 a month $180 is INTEREST

Pay it Off then start putting $ into savings because their is no way you can get a better return on savings to justify the huge amount of interest you are paying.

Message 13 of 22

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

11:27 AM

03-06-2008

11:27 AM

Re: utilization -- pay down or off?

Blah2 wrote:The score would drop because even though your payment history will be reflected on your report from 7-10 years, the account will not have recent "on-time" payments made to it and the account will reflect as paid in full and closed. Doesn't make a whole lot of sense I know, but that is how it works.

Message 14 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

11:35 AM

03-06-2008

11:35 AM

Re: utilization -- pay down or off?

@wvasweetness wrote:

Yep - an auto loan dropping off "suddenly" will definitely mean a hit to your CR. We paid off an ATV 2 years early, which meant a 30-50pt decrease across the board.

It's sickening.

Same thing here. I/we paid of 2 auto loans last July, and scores dropped 32 points.

Message 15 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

11:41 AM

03-06-2008

11:41 AM

Re: utilization -- pay down or off?

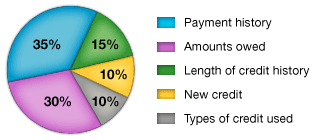

The reason, we suggest NOT paying off a car loan, is that FICO likes to see a mix of different credit instruments, like cc's, mortgage, etc. Revolving and installment the most important issues. The credit mix accounts for 10% of your FICO score. Loosing a component will cause a score drop. Look at the pie chart to see the importance of FICO scoring catagories:.........................

FICO Scores are calculated from a lot of different credit data in your credit report. This data can be grouped into five categories as outlined below. The percentages in the chart reflect how important each of the categories is in determining your FICO score.

I refer to this daily.

Message 16 of 22

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

12:01 PM

03-06-2008

12:01 PM

Re: utilization -- pay down or off?

Sylviatob wrote:The reason, we suggest NOT paying off a car loan, is that FICO likes to see a mix of different credit instruments, like cc's, mortgage, etc. Revolving and installment the most important issues. The credit mix accounts for 10% of your FICO score. Loosing a component will cause a score drop. Look at the pie chart to see the importance of FICO scoring catagories:.........................FICO Scores are calculated from a lot of different credit data in your credit report. This data can be grouped into five categories as outlined below. The percentages in the chart reflect how important each of the categories is in determining your FICO score.

I refer to this daily.

Sylvia, still, the crux of the question is "Does a paid account still facor in to the mix you described above?" The type of TL is still listed on your CR, even for a piad account. My contention is that this still represents a good mix of credit use, even if it is paid off. People should not be fearful of paying off 9% auto loans if there is a more prudent use for the money, or a more prudent way to carry the debt.

I mean, for example, by your own pie chart, "amount owed' carries far more imporetance than "types of credit". Let's not lose sight of the forest for the trees. (And good discussion by the way)

Message Edited by VistaV on 03-06-2008 12:03 PM

Message 17 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

12:11 PM

03-06-2008

12:11 PM

Re: utilization -- pay down or off?

Sorry Vista, not trying to sidestep your question, just trying to get to as many people as I can.

Your payment history will remain on your accont for a full 10 years after payoff..

But it will not be counted in the mix of credit, as you have effectively lost that portion of the mix.

Does that help?

Message 18 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

01:00 PM

03-06-2008

01:00 PM

Re: utilization -- pay down or off?

Great chart/nugget of information...needs to be pinned/saved somewhere for future references...thank you Sylviatob!

Message 19 of 22

0

Kudos

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

03-06-2008

01:40 PM

03-06-2008

01:40 PM

Re: utilization -- pay down or off?

It's in the Credit Education section of the black menu bar under the link "what's in your score".

This website, outside of the fourm, is a wealth of info unto itself.

Message 20 of 22

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.