- myFICO® Forums

- FICO Scoring and Other Credit Topics

- Understanding FICO® Scoring

- Re: Score low and risk high apparently....

Options

- Subscribe to RSS Feed

- Mark Topic as New

- Mark Topic as Read

- Float this Topic for Current User

- Bookmark

- Subscribe

- Mute

- Printer Friendly Page

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Score low and risk high apparently....

Is your credit card giving you the perks you want?

Browse credit cards from a variety of issuers to see if there's a better card for you.

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

12:06 PM

02-29-2020

12:06 PM

Score low and risk high apparently....

As you can see below, there is quite a bit of green, but my score is 640. They say my risk of getting into "serious trouble is 25%. I recently applied for Affirm 0% financing to buy a $1,000 product and was denied.

Obviously I am a high risk borrower, but it seems like from all the Above Average ratings and calculating the percentage impact, that I should be at least average.

EQ671 TU673 EX662

Labels:

Message 1 of 33

32 REPLIES 32

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

12:12 PM

02-29-2020

12:12 PM

Re: Score low and risk high apparently....

I think Affirm is a weird one. They approved me for $2,900 for a Peloton workout machine but only $700 on a virtual card. Walmart is $1,300.

my scores and reports aren't as good as yours

Message 2 of 33

Anonymous

Not applicable

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

12:19 PM

02-29-2020

12:19 PM

Re: Score low and risk high apparently....

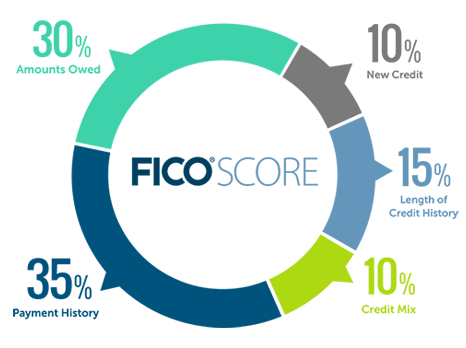

It's because your debt is relatively high considering you have a "fair" rating which counts for 30% of your scores.

Message 3 of 33

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

12:50 PM

02-29-2020

12:50 PM

Re: Score low and risk high apparently....

As noted above, your utilization at 75% had a significant factor in your denial. When seeking credit, it's recommended to optimize your report.

https://www.myfico.com/credit-education/whats-in-your-credit-score

Message 4 of 33

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

02:10 PM

02-29-2020

02:10 PM

Re: Score low and risk high apparently....

Your utilization is very high and that makes you a risky borrower.

If you cannot pay it without getting a personal loan, that right there explains why you're considered a "higher risk" at this time.

With such high utilization, getting a personal loan under anything resembling decent terms is going to be very hard.

You will probably need to make a plan on how to get utilization down a bit to a more manageable levels, then see what you can do personal loan wise.

Message 5 of 33

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

02:19 PM

02-29-2020

02:19 PM

Re: Score low and risk high apparently....

How recent is the 30-day late?

FICO 8: EQ 810; TU 816; EX 822 as of 7/5/2022

Message 6 of 33

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

04:11 PM

02-29-2020

04:11 PM

Re: Score low and risk high apparently....

The 30 day late was from 2018.

The high ratio makes up 30%, but having 70% great seems like it would mean more.

EQ671 TU673 EX662

Message 7 of 33

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

04:55 PM

02-29-2020

04:55 PM

Re: Score low and risk high apparently....

The 30-day late might have a significant effect on your score, though it's possible it does not.

Do you have any other derogatories?

I had a 30-day late which lowered my score about 70 points in 2013....but the effect of it waned considerably in a few months.

75% utilization stifles the score. 60% utilization stifled mine. My score went up over 100 points when I reduced my utilization from 60% to 4%.

FICO 8: EQ 810; TU 816; EX 822 as of 7/5/2022

Message 8 of 33

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

05:16 PM

02-29-2020

05:16 PM

Re: Score low and risk high apparently....

No other derogatory items. If my score was 840, or whatever perfect is, even if the util. Makes up 30% and was as bad as possible, that shouldn't be able to drop it this much. I am no math whiz, but I know this doesn't add up.

EQ671 TU673 EX662

Message 9 of 33

0

Kudos

- Mark as New

- Bookmark

- Subscribe

- Mute

- Subscribe to RSS Feed

- Permalink

- Report Inappropriate Content

02-29-2020

05:17 PM

02-29-2020

05:17 PM

Re: Score low and risk high apparently....

Take heart.....credit cards aren't rushing to have me as a client, either......

FICO 8: EQ 810; TU 816; EX 822 as of 7/5/2022

Message 10 of 33

0

Kudos

† Advertiser Disclosure: The offers that appear on this site are from third party advertisers from whom FICO receives compensation.